How to Invest in Stocks: A Complete Step-by-Step Guide for Beginners

Learning how to invest in stocks is one of the highest-leverage financial skills you can develop. Done correctly, stock investment turns ordinary income into extraordinary long-term wealth through the mathematics of compound returns. Done incorrectly — through emotional trading, stock picking without research, or high-fee products — it burns both money and confidence.

This guide gives you the complete, honest, step-by-step process for investing in stocks as a beginner. No jargon. No shortcuts. No promises of fast money. Just the system used by millions of ordinary investors to build real wealth over time.

💡 Before You Begin: Successful stock investing is not about picking the next Apple or timing market crashes. It’s about consistently putting money into well-diversified, low-cost investment vehicles and leaving it alone long enough for compounding to work. The 7-step process below is based on that principle.

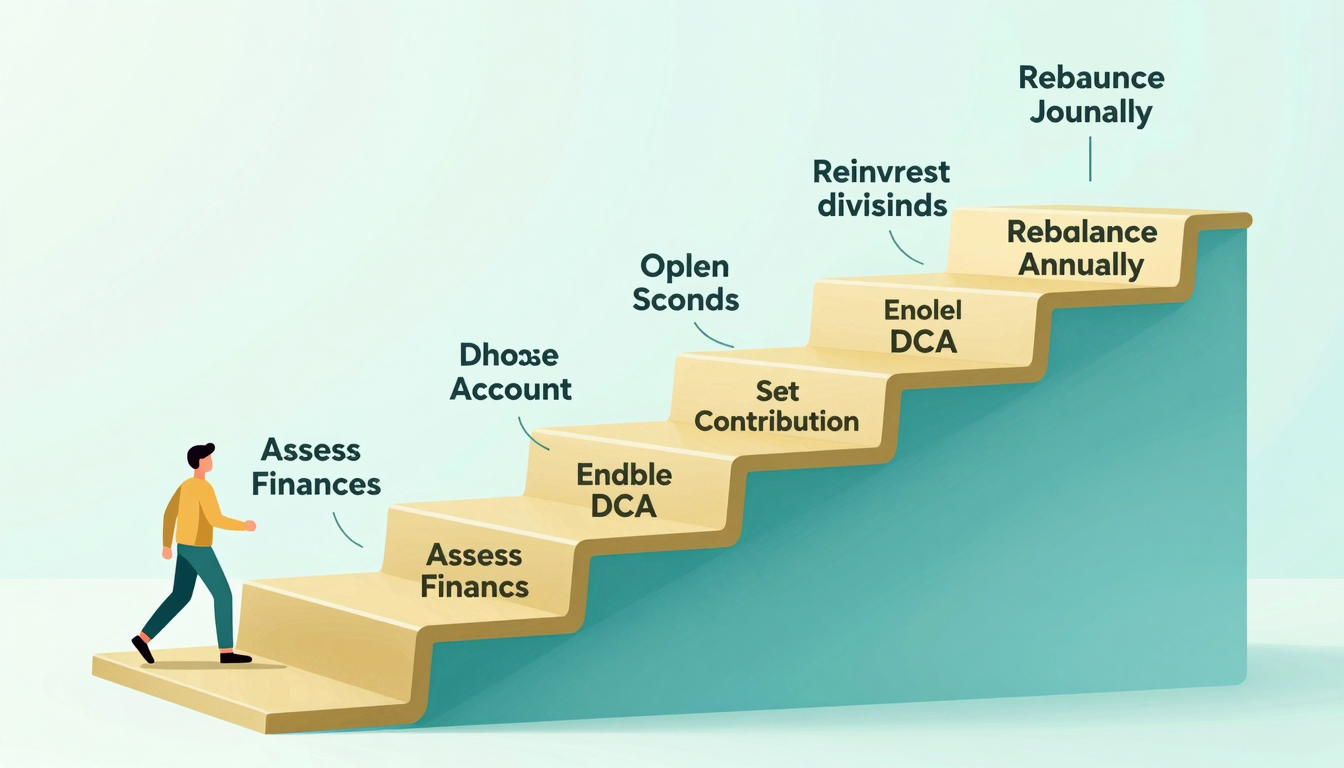

⚡ Quick Summary: 7 Steps to Invest in Stocks

- Assess your financial situation (debt, emergency fund, goals)

- Choose your account type (brokerage, Roth IRA, 401k)

- Open an account with a reputable broker

- Select your investments (index funds for most beginners)

- Deposit money and place your first trade

- Set up automatic recurring investments (dollar-cost averaging)

- Monitor annually — rebalance and stay the course

Step 1: Assess Your Financial Situation First

Before you invest a single dollar in stocks, you need to ensure your financial foundation is solid. Stocks are long-term investments — the money you put into them should be money you don’t need for at least 5 years, ideally 10+. Investing money you might need next year forces you to sell at the worst possible time (usually during market downturns when you’re most financially stressed).

The Financial Foundation Checklist

| Prerequisite | Target | Why It Matters |

|---|---|---|

| Emergency fund | 3–6 months expenses in savings | Prevents forced selling during downturns |

| High-interest debt | Zero credit card / personal loan debt above 7% | 10% stock return means nothing if paying 18% on debt |

| Employer 401k match | Contribute enough to capture full match | Free 50–100% instant return on contributions |

| Investment timeline | 5+ years before you need the money | Stocks can decline 40%+ short-term; time heals |

If you have high-interest debt, pay it off before investing in stocks. A credit card charging 22% interest is a guaranteed 22% loss on every dollar that stays on the card. No stock investment offers a reliable 22% return. Eliminate that debt first, then redirect those payments into investments.

Step 2: Choose Your Account Type

This is the most important tax decision you’ll make as an investor. Different account types have different tax advantages, contribution limits, and withdrawal rules. Choosing the wrong account type can cost you tens of thousands of dollars over a lifetime.

Account Types Explained

| Account Type | Tax Treatment | 2024 Limit | Best For |

|---|---|---|---|

| 401(k) | Pre-tax (pay tax on withdrawal) | $23,000 | First priority (especially with employer match) |

| Roth IRA | After-tax (withdrawals tax-free) | $7,000 | Second priority; best for long-term compounders |

| Traditional IRA | Pre-tax (pay tax on withdrawal) | $7,000 | Alternative to Roth if expecting lower tax bracket in retirement |

| Taxable Brokerage | No tax advantages; pay capital gains tax | Unlimited | After maxing tax-advantaged accounts; flexible |

The recommended priority order:

- 401(k) up to employer match (free money first)

- Roth IRA up to annual limit ($7,000 in 2024)

- Back to 401(k) up to annual limit ($23,000)

- Taxable brokerage for additional savings

The Roth IRA is particularly powerful for younger investors. You contribute after-tax dollars, but all growth and withdrawals in retirement are completely tax-free. If you invest $7,000/year in a Roth IRA for 30 years with 10% average returns, you accumulate over $1.2 million — and every dollar of withdrawal in retirement is tax-free income.

Step 3: Open a Brokerage Account

Opening a brokerage account is simpler than opening a bank account. The entire process takes 5-15 minutes online. Here’s what to look for and how to do it.

What to Look for in a Broker

- Zero commission on stock and ETF trades — All major brokers offer this now. Non-negotiable.

- No account minimum — You should be able to open with any amount

- Access to index funds and ETFs — Particularly their own low-cost index funds

- SIPC insurance — Protects your account up to $500,000 if the brokerage fails

- Fractional shares — Ability to buy partial shares of expensive stocks like Amazon or Google

Top Brokers for Beginners

| Broker | Best Feature | Signature Fund | Account Min |

|---|---|---|---|

| Fidelity | Best overall; ZERO fee index funds | FZROX (0.00% ER) | $0 |

| Vanguard | Pioneer of index investing; investor-owned | VTSAX (0.04% ER) | $0 ETF / $3,000 mutual fund |

| Charles Schwab | Excellent research tools; fractional shares | SCHB (0.03% ER) | $0 |

| Interactive Brokers | Best for international investors | Access to global markets | $0 |

For most US-based beginners, Fidelity is the best choice — zero-fee index funds (literally 0.00% expense ratio), no account minimum, excellent mobile app, and outstanding customer service.

For international investors, Interactive Brokers offers the best combination of low fees, global market access, and regulatory coverage across 150+ countries.

Opening Your Account: Step by Step

- Visit the broker’s website and click “Open an Account”

- Choose your account type (Individual Brokerage or Roth IRA for most beginners)

- Enter personal information: name, address, Social Security Number (for US residents), date of birth

- Answer suitability questions about your investment experience and goals

- Link your bank account for transfers

- Verify your identity (upload ID photo in most cases)

- Wait 1-3 business days for approval

Step 4: Select Your Investments

This is where most beginners overthink. The research is clear: for most investors, a simple two or three-fund portfolio of low-cost index ETFs outperforms complex actively managed strategies over the long run.

The Simple Two-Fund Portfolio (Recommended for Most Beginners)

- 70-80%: US total market fund — VOO (S&P 500), VTI (US total market), or FZROX (zero fee)

- 20-30%: International fund — VXUS (international total market) or FZILX

That’s it. Two funds. Rebalance once a year. This portfolio holds thousands of companies across the entire global economy. You own a slice of everything.

✅ Why This Works: Vanguard’s research shows that the global stock portfolio (US + international stocks, market-cap weighted) captures essentially all the risk premium available to equity investors. Adding bonds reduces volatility but also expected returns. For young investors with decades ahead, keeping it in stocks maximizes long-term wealth accumulation.

Adding Bonds for Stability

If you’re over 50, closer to retirement, or simply can’t stomach watching your portfolio drop 40% during bear markets, add a bond allocation:

- Age 30-40: 80% stocks / 20% bonds (AGG or BND)

- Age 40-50: 70% stocks / 30% bonds

- Age 50-60: 60% stocks / 40% bonds

- Retirement: 40-50% stocks / 50-60% bonds

Bonds act as shock absorbers — they tend to hold value or even rise during stock market crashes, giving you stability and rebalancing fuel when stocks are cheap.

Step 5: Place Your First Trade

Once your account is funded, placing your first trade is straightforward. Log into your broker, search for the ETF symbol (e.g., “VOO”), and click “Buy.” You’ll see:

- Market order: Buy immediately at the current price. Fine for most investors.

- Limit order: Specify the maximum price you’ll pay. Useful for individual stocks, rarely necessary for ETFs.

- Number of shares: How many units to purchase. If you have $1,000 and VOO is $480/share, buy 2 shares (if fractional shares available, you can invest the exact dollar amount).

Click “Review Order,” confirm the details, and submit. Your first stock investment is complete. The transaction settles in 1-2 business days, and the shares will appear in your account.

Step 6: Set Up Automatic Recurring Investments

The most important habit in stock investing is consistency. Set up automatic monthly transfers from your bank account to your brokerage account, then automatic monthly purchases of your target funds.

Most modern brokers support automatic investing — you set it up once and it runs indefinitely without any action from you. This implements dollar-cost averaging automatically: you invest $500 (or whatever amount) monthly regardless of market conditions.

The mathematical impact of consistency:

| Monthly Investment | 10 Years (10% returns) | 20 Years | 30 Years |

|---|---|---|---|

| $200/month | $38,600 | $151,900 | $452,000 |

| $500/month | $96,500 | $379,700 | $1,131,000 |

| $1,000/month | $193,000 | $759,400 | $2,261,000 |

| $2,000/month | $386,000 | $1,518,800 | $4,522,000 |

Notice: the jump from 20 years to 30 years is much larger than the jump from 10 to 20. This is compounding’s hockey-stick effect. Every year you stay invested, the growth accelerates.

Step 7: Annual Review and Rebalancing

Once per year — on New Year’s Day, your birthday, or any fixed date — review your portfolio. This review has three goals:

- Check allocation: Has your US/international split drifted significantly from your target? If target is 75/25 but now it’s 82/18, rebalance.

- Increase contributions: Have you received a raise? Increase monthly contributions by 50% of the raise.

- Stay the course: Confirm you’re not making emotional decisions based on recent market performance.

Rebalancing is mechanical: sell the outperformer (which is now “expensive”), buy the underperformer (which is now “cheap”). This is the opposite of what emotions tell you to do — which is exactly why the rule exists.

In tax-advantaged accounts, rebalancing has no tax consequences. In taxable brokerage accounts, you can often rebalance by directing new contributions to the underweight asset rather than selling, which avoids triggering capital gains.

⛔ The One Rule That Overrides Everything: Do not sell during market crashes. In 2009 (after 50% crash), investors who sold locked in catastrophic losses. Investors who held — or bought more — made everything back within 3 years and went on to triple their money in the next decade. Market crashes are temporary. Selling at the bottom is permanent.

🎓 What to Do When You’re More Confident

After 1-2 years of consistent investing with a simple index fund portfolio, you might feel ready to explore more. Here are sensible next steps — in order of recommendation:

1. Optimize tax efficiency: Learn asset location (which investments belong in which account type for maximum after-tax returns). This is free money through tax optimization.

2. Add a factor tilt: Research suggests value stocks and small-cap stocks have historically delivered premium returns. Adding a small allocation (10-20%) to VBR (Vanguard Small Cap Value) or AVUV (Avantis US Small Cap Value) can enhance long-term returns.

3. Individual stocks (as a satellite): If you want to research and own individual company stocks, keep it to 10% or less of your portfolio. Treat it as the speculative satellite around your passive core. Never let individual stock picking become more than 10-15% of your total investment.

4. Real estate through REITs: Adding 5-10% in a REIT index fund (VNQ) provides real estate exposure with the liquidity of stocks.

But here’s the honest truth: none of these additions will meaningfully outperform the simple two-fund portfolio for most investors. Simplicity wins. The marginal return of complexity rarely justifies the additional cognitive load and trading costs.

🚨 The 7 Biggest Mistakes New Investors Make

1. Waiting for the “right time” — Markets are at all-time highs frequently. If you wait for a crash, you might wait 10 years and miss massive gains. The best time to invest was yesterday. The second best time is today.

2. Checking your portfolio daily — This is how emotion destroys strategy. Daily checking leads to reactive trading. Check monthly at most; annually is better.

3. Trying to pick individual winning stocks — 95% of professional fund managers fail to beat the S&P 500 index over 20 years. Your odds are worse. Use index funds.

4. Chasing performance — Last year’s top-performing sector almost always underperforms next year. Don’t buy what already ran. Stick to your allocation.

5. Paying high fees — A 1% annual fee sounds small. Over 30 years on a $100,000 investment, it costs you over $100,000 in lost compounding. Use funds with expense ratios under 0.10%.

6. Selling during crashes — This is the most expensive mistake. It turns temporary paper losses into permanent real losses, and means you miss the recovery. Hold through volatility.

7. Not investing at all — Every year you wait is a year of compounding you’ll never get back. A 25-year-old who starts investing has a massive structural advantage over a 35-year-old who waits “until things are more stable.” Imperfect investing started early beats perfect investing started late.

❓ Frequently Asked Questions

How do I know which stocks to buy as a beginner?

Don’t pick individual stocks as a beginner. Buy a total market index fund like VTI or VOO. These automatically include hundreds of companies, and you participate in all their growth without needing to research individual companies. As you gain experience, you can explore individual stocks — but keep any individual stock positions under 10% of your portfolio.

How much should I invest monthly?

As much as you can consistently sustain without lifestyle sacrifice. Even $100-200/month is meaningful when started early. The rule of thumb: save and invest 15-20% of gross income. If that’s not possible yet, start wherever you can and increase as income grows.

What happens if the market crashes right after I start?

This is actually the best possible scenario for a long-term investor who’s just starting out. A market crash means you can buy shares at discounted prices for months or years. Every $500 monthly contribution buys more shares when prices are lower. Crashes hurt people who are about to retire; they help people who have decades ahead.

Do I need a financial advisor?

Most beginners do not. A simple two-fund index portfolio is straightforward enough to manage independently. If your situation is complex (business owner, stock options, significant inheritance, divorce), a fee-only fiduciary financial advisor (who charges a flat fee, not a percentage of assets) is worth consulting. Avoid advisors who earn commissions from selling products.

Should I invest or pay down my mortgage?

If your mortgage interest rate is below 6-7%, invest first (expected stock returns exceed the mortgage rate). If your mortgage rate is above 7%, paying down debt first offers a guaranteed return equal to your interest rate. Many people split the difference: invest enough to capture employer match, then pay down mortgage.

Your Action Plan for This Week

1. Open a Roth IRA or brokerage account at Fidelity or Vanguard

2. Fund it with whatever you can — even $100 to start

3. Buy VOO or VTI

4. Set up $200-$500 automatic monthly investment

5. Don’t touch it for 20 years

Related reading: What is stock investment · Stock investment strategies · How to open a brokerage account · Dollar cost averaging guide · Stock market for beginners

🔬 Deep Dive: The Psychology of Consistent Investing

Knowing how to invest in stocks is the easy part. The hard part is the behavioral component — maintaining your investment discipline when markets are volatile, your friends are bragging about winning crypto bets, and every news headline is announcing imminent economic catastrophe.

Understanding the psychology of successful investing prepares you for the emotional challenges ahead.

Why Your Brain Is a Bad Stock Market Investor

Human brains evolved for survival in short-term, high-stakes environments. We’re wired to avoid loss more than we pursue gain (loss aversion), to base decisions on recent events (recency bias), and to follow the crowd (herd behavior). These instincts kept our ancestors alive on savannas. They destroy investment portfolios.

Loss aversion in practice: Research by Kahneman and Tversky shows that the psychological pain of losing $1,000 is approximately twice as powerful as the pleasure of gaining $1,000. This means a 20% market drop feels emotionally devastating — creating a powerful urge to sell and “stop the pain” — even when holding is the mathematically correct decision.

Recency bias in practice: After a 3-year bull market, investors extrapolate that stocks “always go up” and overinvest at peaks. After a crash, they extrapolate that stocks “always go down” and sell at bottoms. Both are reacting to recent events rather than the long-term probabilistic view.

Herd behavior in practice: When everyone around you is making money on meme stocks, crypto, or some hot sector ETF, social pressure to participate can feel overwhelming. FOMO (Fear of Missing Out) drives investors to abandon diversified, boring index funds for exciting concentrated bets — almost always at peak valuations, after most of the gains are already made.

Behavioral Systems That Override Emotion

The solution isn’t trying to suppress emotions (impossible). It’s designing systems that remove emotion from the investing process:

Automation: Automatic monthly investments mean you don’t decide each month whether the market “looks right.” The decision was made once, rationally, when you set up the automatic transfer. Every subsequent investment happens without a new emotional decision point.

Rules-based rebalancing: Rebalance when allocations drift beyond 5% from target (e.g., you target 70/30 US/international; rebalance when it hits 75/25 or 65/35). This removes the subjective “should I rebalance now?” question.

Cooling-off periods: If you feel the urge to make a portfolio change (sell everything, move to cash, buy into the hot sector), impose a 7-day rule. Write down your reasoning, put it in a drawer, and revisit after 7 days. Most panic-driven decisions don’t survive a week of reflection.

Investment policy statement: Write a one-page document stating your target allocation, rebalancing rules, contribution schedule, and investment philosophy. Review it when markets are volatile. Seeing your own written rationale, created when you were calm, provides an anchor against impulsive decisions.

The Two Events That Will Test Your Discipline

Event 1 — The bear market: At some point in your investing life, markets will fall 30-50%. Your portfolio balance will drop significantly. Every media outlet will declare a financial crisis. Friends and family will advise you to “just move to cash until things stabilize.” This is the moment that separates long-term wealth builders from people who perpetually try to catch up.

Historically: every US market decline (including the Great Depression, 2008 Financial Crisis, and COVID crash) has been followed by a full recovery and new all-time highs. Investors who held earned excellent long-term returns. Investors who sold and tried to “time the reentry” typically missed the recovery’s best days (which cluster at the beginning of recoveries, when sentiment is still terrible).

Event 2 — The speculative bubble: During your investing life, at least one asset class will deliver extraordinary returns for 2-5 years, attracting massive media attention and social comparison pressure. Bitcoin in 2017 and 2021, cannabis stocks in 2018, tech stocks in 1999, meme stocks in 2021. Every bubble looks obvious in retrospect and compelling in the middle.

The prescription: allow yourself a small “exploration” allocation (5% maximum) if you feel compelled to participate. Keep the other 95% in your boring diversified index funds. This reduces FOMO while protecting the core portfolio from catastrophic loss when the bubble inevitably deflates.

📊 Real Numbers: What Consistent Investing Actually Produces

Abstract percentages don’t inspire action. Concrete dollar projections do. Here is what realistic, consistent stock investment produces at the individual level — based on historical S&P 500 returns of approximately 10% annually (7% real returns after inflation).

Scenario A: The Early Starter

Age 22. Invests $300/month. Never increases contributions. Stops at age 62 (40 years). Final portfolio: approximately $1.59 million. Total contributed: $144,000. Growth from compounding: $1.45 million. Market return did 10x the work of the investor’s contributions.

Scenario B: The Late Starter

Age 32. Invests $300/month for 30 years. Final portfolio at 62: approximately $603,000. Same monthly contribution, 10 years later start: ends up with $986,000 less. The 10-year delay cost nearly a million dollars. Time truly is the most valuable input in investing.

Scenario C: The Consistent Increaser

Age 25. Starts with $200/month, increases by $50/month every 5 years as career grows. At retirement age 65: approximately $2.1 million. This is the “invest and grow contributions with your career” approach — the most realistic for most people.

The message in all three scenarios: start as early as possible, contribute consistently, and increase contributions as income grows. The specific investment vehicle (which index fund) matters far less than these three behavioral habits.

Once your account is open, the next step is deciding which stock investment strategy fits your goals — value, growth, dividend, or index investing each has distinct advantages worth understanding.

New to investing altogether? Our comprehensive stock market guide for beginners explains how the market works, why prices move, and the key concepts to know before your first investment.

Leave a Reply