In 1965, a young Warren Buffett bought shares in a struggling textile company called Berkshire Hathaway. He later called it one of his worst investments — not because it failed, but because he bought a cheap, declining business instead of a great, growing one. That lesson shaped his evolution into what he eventually became: an investor who understood that the future belongs to businesses that compound.

Growth investing is the philosophy built on that insight. This guide explains what it is, how it works, how to identify genuinely great growth companies, and how to avoid the most expensive mistakes growth investors make — including mistaking hype for compounding.

💡 What Is Growth Investing?

Growth investing is an investment strategy that focuses on companies expected to grow revenues and earnings significantly faster than the overall market — and buys shares in those companies with the expectation that superior earnings growth will drive superior long-term share price appreciation.

Unlike value investing — which focuses on buying what’s cheap relative to current earnings — growth investing focuses on future potential. A growth investor is willing to pay a premium today for a business that will be worth dramatically more in 5–10 years. The question isn’t “is this stock cheap?” but “will this business be dramatically larger and more profitable in the future?”

When growth investors are right, the returns are extraordinary. Amazon, Apple, Google, Netflix — investors who identified these companies early and held through volatility created generational wealth. When growth investors are wrong — paying too much for companies that don’t deliver the promised growth — the losses can be equally dramatic.

📈 The Compounding Machine: Why Growth Investing Works

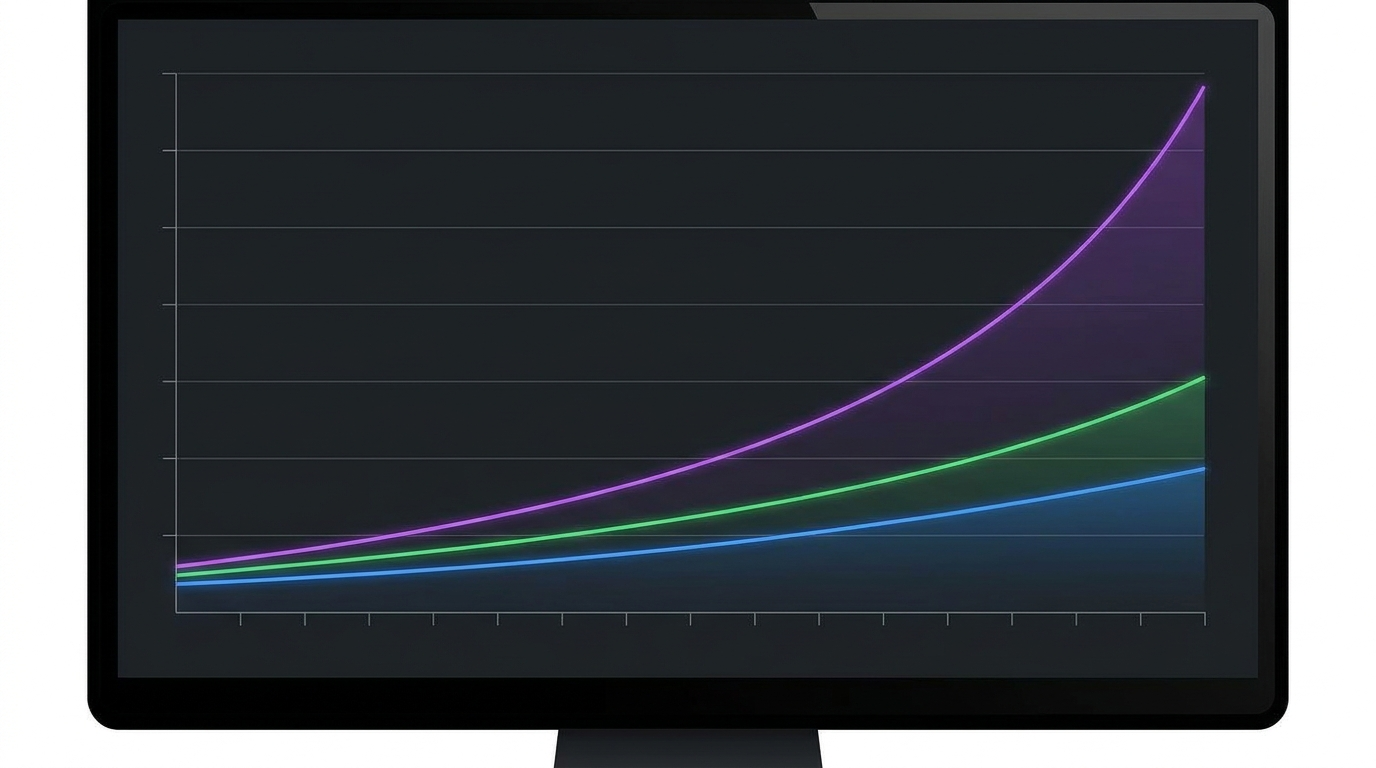

The mathematical foundation of growth investing is compounding — specifically, the compounding of earnings and revenue rather than just price.

A company growing earnings at 25% annually doubles them every 3 years. In 10 years, earnings are 9.3x the starting point. If the market applies the same earnings multiple, the stock price also rises 9.3x. Add in potential multiple expansion as investors increasingly recognize the company’s quality, and returns can be even higher.

This is why early investors in exceptional growth companies — those who identified Microsoft in 1990, Amazon in 2002, or Apple in 2008 — generated returns that no value investing approach could match. The compounding of business quality at high rates over long periods produces asymmetric returns unavailable elsewhere.

The challenge: identifying genuine compounders before the market prices in their potential. Paying 100x earnings for a company that delivers 30% growth for 10 years produces extraordinary returns. Paying 100x earnings for a company that delivers 15% growth for 3 years before stalling produces significant losses.

🔍 What Makes a True Growth Company?

Not every fast-growing company is a good growth investment. These are the characteristics that separate genuine compounders from growth stories that fizzle:

1. Large Total Addressable Market (TAM)

A company can only grow as large as its market allows. The most exceptional growth companies address markets so large that even capturing a small fraction represents massive absolute revenue. Amazon’s early focus on e-commerce tapped a retail market measured in trillions globally. Salesforce’s focus on CRM software addressed an enterprise software market that dwarfed its early revenue many times over.

Be suspicious of companies claiming enormous TAMs while showing limited actual penetration. TAM analysis requires realistic assessment of actual addressable customers, not theoretical maximum market sizes.

2. Durable Competitive Advantage

High growth attracts competition. The growth companies that continue compounding for decades do so because they build competitive advantages that protect margins and market share as they scale. Network effects (more users → more valuable), switching costs (hard to leave → customers stay), and brand loyalty (trust → pricing power) are the most durable advantages in growth businesses.

A company growing 40% annually with no competitive moat is a temporary opportunity. A company growing 25% annually with deepening competitive advantages is a potential multi-decade compounder.

3. Scalable Business Model

The best growth businesses can scale revenue dramatically without proportionally scaling costs. Software is the canonical example: writing code once and selling it to millions of customers costs almost nothing incremental after development. Each additional customer is nearly pure margin. Contrast this with a restaurant chain — adding revenue requires adding physical locations, staff, and inventory at proportional cost.

Gross margin expansion as companies scale is the financial signature of genuinely scalable business models. A software company growing from 60% to 75% gross margins as it scales is demonstrating the economic power of its model. A company whose margins compress as it grows is revealing structural cost challenges that will limit ultimate profitability.

4. Founder-Led or Mission-Driven Management

Extraordinary growth companies are disproportionately built by extraordinary founders or mission-driven leaders who think in decades rather than quarters. Bezos’s relentless long-term focus, Jobs’s product obsession, Zuckerberg’s willingness to sacrifice short-term profits for platform growth — these leadership characteristics are difficult to quantify but enormously consequential.

Look for management teams that own significant equity (aligned with shareholders), have long track records of executing on stated plans, reinvest aggressively in future growth rather than extracting cash, and communicate honestly about both strengths and challenges.

5. Recurring Revenue

Subscription and recurring revenue models create predictable, compounding revenue streams that one-time sale models can’t match. A SaaS company with 90% annual revenue retention (customers renewing at $0.90 for every $1.00 they spent last year) starts each year with a predictable base before adding any new customers. This visibility into future revenue makes forecasting more reliable and compounding more consistent.

6. Expanding Margins Over Time

As great growth companies scale, their operating leverage kicks in — fixed costs spread over larger revenue bases, improving profit margins. A company consistently expanding operating margins while growing revenue demonstrates genuine business quality. Companies where margins persistently compress as revenue grows often have structural cost problems that will eventually cap profitability.

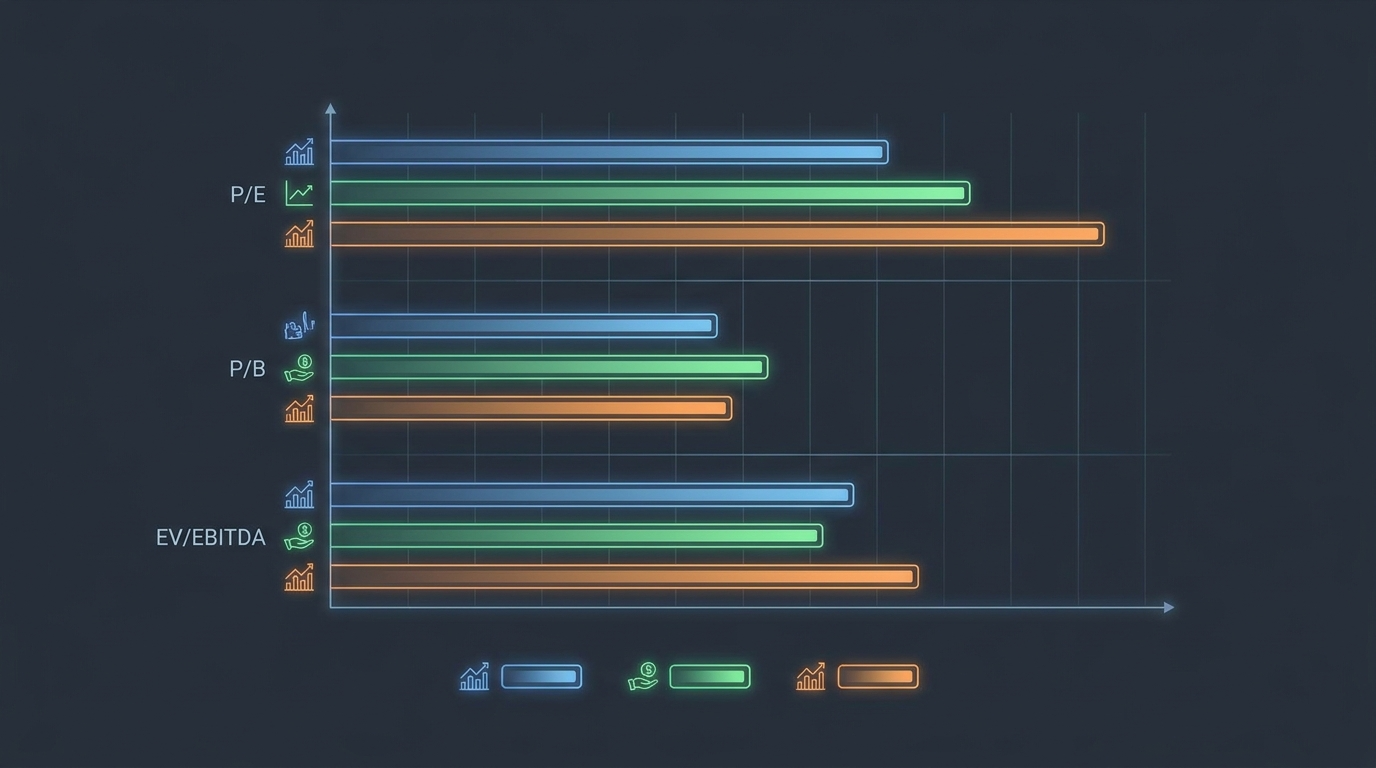

📊 Key Metrics for Growth Investors

Growth investing uses a different analytical toolkit than value investing. These are the metrics that matter most:

Revenue Growth Rate

The most fundamental metric. Consistent, accelerating, or even decelerating-but-still-high revenue growth is the first filter. Early-stage growth companies often prioritize revenue growth over profitability — understanding why and whether the underlying economics support eventual profitability is the analytical challenge.

Gross Margin

Revenue minus cost of goods sold, expressed as a percentage. Gross margin reveals the inherent profitability of the core business before operating expenses. Software businesses with 70–80%+ gross margins have fundamentally different economics than hardware or retail businesses with 30–40% margins. High, stable, or expanding gross margins are a prerequisite for eventual high profitability.

Net Revenue Retention (NRR)

For subscription businesses: what percentage of last year’s revenue do existing customers generate this year, including expansions and subtracting churn? NRR above 120% means existing customers alone generate 20% more revenue each year before adding any new customers — a powerful compounding mechanism. The best SaaS companies achieve 130–150% NRR.

Customer Acquisition Cost (CAC) vs. Lifetime Value (LTV)

How much does it cost to acquire a customer versus how much revenue that customer generates over their lifetime? LTV:CAC ratios above 3:1 indicate efficient growth — the business generates at least $3 of lifetime value for every $1 spent acquiring customers. Companies with LTV:CAC below 1:1 are destroying value with every customer acquired, regardless of revenue growth rates.

Price-to-Earnings Growth (PEG Ratio)

Developed by Peter Lynch: P/E ratio divided by earnings growth rate. A company with a P/E of 30 growing earnings at 30% has a PEG of 1.0 — often considered fairly valued for a growth company. PEG below 1.0 may indicate undervaluation; above 2.0 suggests the market is pricing in very high growth expectations that create significant downside risk if growth disappoints.

Rule of 40

For software companies: revenue growth rate + profit margin should exceed 40%. A company growing 35% with 10% profit margins scores 45 — healthy. A company growing 20% with -10% margins scores 10 — burning cash without sufficient growth to justify it. The Rule of 40 balances growth and profitability into a single efficiency metric.

Free Cash Flow Conversion

Eventually, growth companies must convert accounting profits (and ultimately growth) into real free cash flow. Companies with high earnings but low free cash flow conversion (due to aggressive revenue recognition, high capital expenditure requirements, or working capital consumption) are often less valuable than their income statements suggest.

🚀 Growth Investing Styles: From Conservative to Aggressive

Growth investing isn’t monolithic — different investors apply the philosophy with different levels of risk tolerance and time horizon:

Quality Growth (GARP — Growth at a Reasonable Price)

Buy high-quality companies with durable competitive advantages and consistent earnings growth at valuations that offer a reasonable margin of safety. This is Buffett’s evolved approach — companies like Coca-Cola in the 1980s, Apple in the 2010s. Lower upside than aggressive growth, but dramatically lower risk of permanent capital loss.

Momentum Growth

Buy companies with strong recent performance metrics (accelerating revenue growth, expanding margins, positive earnings surprises) with the expectation that momentum continues. Higher turnover, higher risk, more sensitive to market sentiment shifts. Works best in bull markets; prone to sharp reversals when growth disappoints or sentiment changes.

Early-Stage Growth (Venture-Style Public Investing)

Buy companies in the earliest stages of their growth trajectory — pre-profitability, often pre-revenue maturity — with outsized future potential. Requires accepting high uncertainty and potential total loss in individual positions in exchange for the possibility of 10–100x returns on the winners. Demands a portfolio approach: accept that 40% of positions may go to zero while 20% deliver extraordinary returns.

Emerging Market Growth

Apply growth investing principles to companies in high-growth economies where market penetration rates remain low. Rising middle classes, digitization of previously cash-based economies, and infrastructure buildout can drive exceptional corporate growth over long periods. Adds political, currency, and governance risk to traditional growth investing risks.

⚠️ Growth Investing Risks and How to Manage Them

Growth investing can produce extraordinary returns — and extraordinary losses. Understanding the specific risks is the first step to managing them:

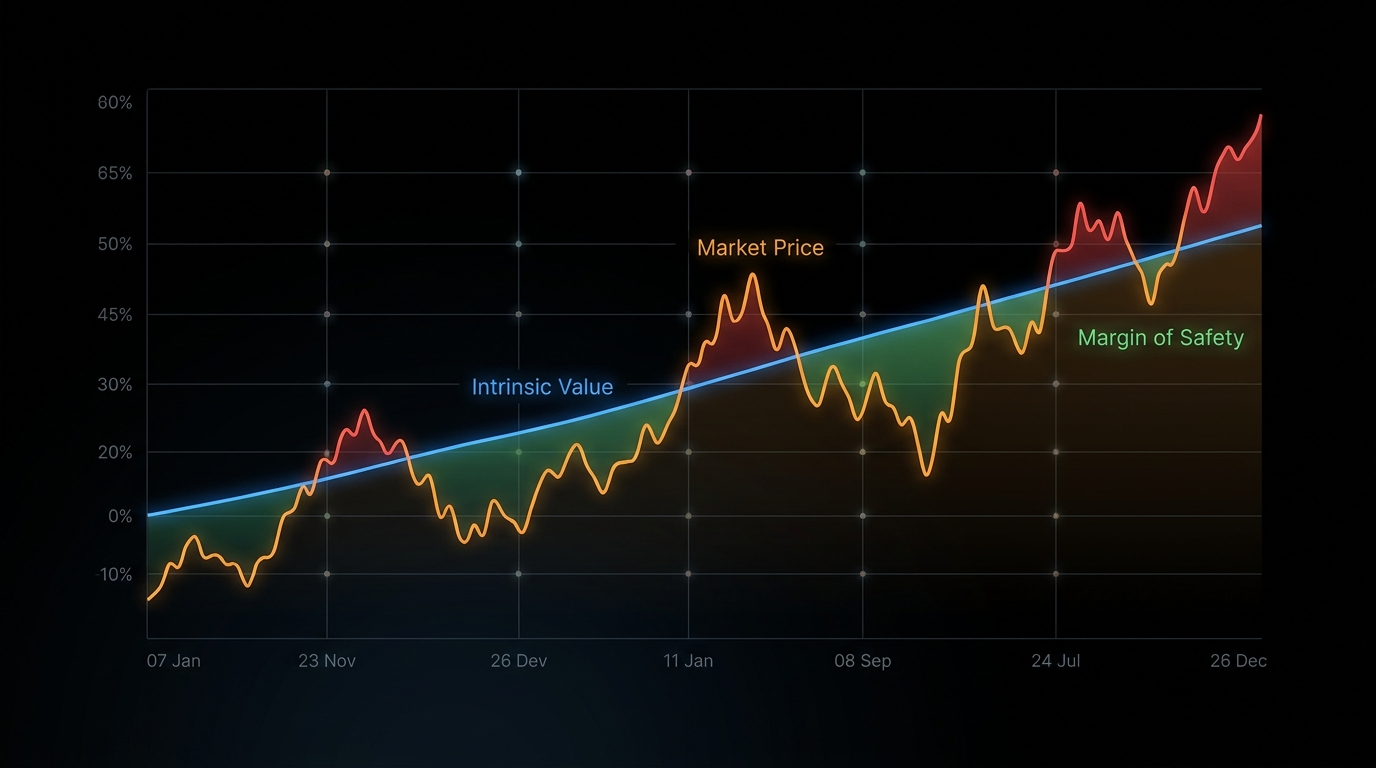

Valuation Risk

High-growth companies often trade at high valuation multiples — 40x, 60x, even 100x earnings. These valuations embed significant future growth expectations. When growth disappoints — or when interest rates rise (making future earnings worth less in present value terms) — high-multiple stocks can fall 50–80% even if the underlying business remains solid. This happened during 2021–2022: many high-quality growth companies fell 60–80% primarily due to multiple compression as rates rose, not business deterioration.

Management: Never invest your entire portfolio in high-multiple growth stocks. Diversify across valuation ranges and business maturity levels. Accept that even great growth companies have periods of significant price decline.

Growth Plateau Risk

Most companies eventually exhaust their primary growth opportunity. The S-curve of business growth — rapid early expansion followed by slowing as markets saturate — is nearly universal. Growth investors who don’t recognize when a company is approaching its growth ceiling often hold too long, sitting through significant multiple compression as the market reprices the company from “growth” to “mature” valuation levels.

Management: Monitor TAM penetration rates. When a company has captured 30–40%+ of its addressable market, growth rates will structurally slow regardless of execution quality. Begin reassessing valuation as growth rates decelerate.

Competition Risk

High margins attract competition. Industries that appear to have permanent growth characteristics can be disrupted by new entrants with superior technology, lower cost structures, or better products. The graveyard of former high-growth companies destroyed by competition — BlackBerry, MySpace, Blockbuster, Kodak — is a reminder that competitive moats require constant reassessment.

Execution Risk

Great business models require great execution. Leadership changes, product missteps, failed acquisitions, and operational challenges can derail even fundamentally sound growth companies. This is why management quality assessment is so critical in growth investing — the people executing the strategy matter enormously.

🚀 Find Your Next Growth Stock

Growth Companies Are Everywhere. Knowing Which Ones Last Is the Edge.

Our full stock investment guides give you the framework to find great companies, evaluate their durability, and build a portfolio that compounds over decades.

📚 Legendary Growth Investors and Their Approaches

Peter Lynch: Managed Fidelity’s Magellan Fund from 1977–1990, averaging 29.2% annual returns. Lynch’s approach: invest in what you know, look for “10-baggers” (stocks that increase 10x), and study every company thoroughly before investing. His books — One Up on Wall Street and Beating the Street — remain essential growth investing texts.

Philip Fisher: Wrote Common Stocks and Uncommon Profits (1958), arguably the founding document of quality growth investing. Fisher’s “scuttlebutt” method — talking to customers, competitors, suppliers, and employees to understand a company’s competitive position — influenced Buffett enormously. Fisher held Amazon-like conviction: buy the best companies and hold them for decades.

Cathie Wood: ARK Invest’s founder represents the modern extreme of high-conviction, early-stage growth investing. Her concentrated bets on disruptive technology companies produced extraordinary returns in 2020 and dramatic losses in 2021–2022. Wood’s approach illustrates both the upside and downside volatility of aggressive early-stage growth investing.

Terry Smith: Fundsmith’s founder applies a quality-growth framework: buy good companies, don’t overpay, do nothing. Smith’s Fundsmith Equity Fund has outperformed global markets over a decade by focusing on businesses with high returns on capital, durable competitive advantages, and reasonable valuations — demonstrating that quality growth and valuation discipline are compatible.

🔄 Growth Investing vs. Value Investing: The False Dichotomy

The debate between growth and value investing is largely artificial. Buffett — the world’s most famous value investor — built his fortune primarily through growth companies: Coca-Cola, American Express, Apple. The distinction that matters isn’t growth vs. value but quality vs. mediocrity and paying a fair price vs. overpaying.

All investing is value investing at its core — you’re always comparing what you pay to what you get. The question growth investors ask is: “what will this business be worth in 10 years?” The question traditional value investors ask is: “what is this business worth today?” Both are legitimate questions. The best investors ask both.

For a complete framework comparing all major investment styles, see our comprehensive guide on stock investment strategies. For understanding the value investing approach and how it complements growth thinking, read our guide on value investing. And for building the portfolio that holds your growth investments alongside other assets, our pillar resource on what stock investment is provides the broader context.

✅ Key Takeaways

- 🔹 Growth investing focuses on companies expected to grow significantly faster than the market — paying premium prices for future earnings power

- 🔹 The compounding of high-quality business growth over long periods produces asymmetric returns unavailable in most other investment approaches

- 🔹 True growth companies have large TAMs, durable competitive advantages, scalable models, and expanding margins

- 🔹 Key metrics: revenue growth rate, gross margin, NRR, LTV:CAC, PEG ratio, Rule of 40, free cash flow conversion

- 🔹 Growth investors range from conservative GARP investors to aggressive early-stage investors — risk and return scale together

- 🔹 Biggest risks: valuation risk from multiple compression, growth plateau, competition, and execution failures

- 🔹 Growth and value investing are not opposites — the best investors combine forward-looking growth analysis with valuation discipline

- 🔹 Never confuse a compelling growth narrative with verified business fundamentals — always check the numbers

❓ Frequently Asked Questions

How do I find growth stocks to invest in?

Start with stock screeners filtering for consistent revenue growth above 20%, expanding gross margins, and positive free cash flow (or a clear path to it). Sector focus matters: technology, healthcare, and consumer discretionary have historically produced the most growth investing opportunities. Beyond screening, follow industry publications, earnings calls, and competitor analysis to understand which companies are genuinely winning in their markets versus just growing into a rising tide.

How long should I hold growth stocks?

The optimal holding period for genuine growth compounders is as long as the competitive advantages remain intact and valuations remain reasonable. Lynch’s 10-baggers took years to develop. Buffett has held Coca-Cola since 1988. Short-term holding periods eliminate most of the compounding benefit and generate unnecessary transaction costs and taxes. That said, when the investment thesis changes — growth is structurally slowing, competition is winning, or management is deteriorating — holding for its own sake is not a virtue.

Should beginners try growth investing?

Growth investing requires more analysis than index investing and more forward-looking judgment than traditional value investing. For true beginners, a core portfolio of broad index ETFs provides growth exposure without requiring individual company selection. As you develop analytical skills and market understanding, adding selective growth positions to a core index portfolio is a rational progression. Jumping directly into concentrated early-stage growth investing without analytical foundation typically produces expensive lessons.

What’s the difference between growth investing and speculation?

The distinction lies in analytical foundation. Genuine growth investing is grounded in business analysis: understanding why a specific company will grow faster than competitors, what competitive advantages protect that growth, and whether the current valuation offers an acceptable risk-adjusted return. Speculation is buying because price has gone up, because others are excited, or because a narrative sounds compelling — without verifying the underlying business fundamentals. Many investors who believe they’re growth investing are actually speculating on narrative momentum.

🌍 Sectors That Produce the Most Growth Companies

While growth companies exist in every sector, certain industries have historically produced a disproportionate share of exceptional long-term growth compounders. Understanding why helps you focus your research where the highest-probability opportunities concentrate.

Technology

Software, semiconductors, cloud computing, and internet platforms have generated the majority of the world’s greatest growth stocks over the past three decades. The reason is structural: technology businesses benefit from near-zero marginal costs (software can be copied for free), global markets accessible from day one, powerful network effects, and rapid innovation cycles that allow category leaders to maintain dominance through constant product improvement. The risk: technology also moves fastest, making last decade’s leader potentially obsolete by the next.

Healthcare and Biotechnology

Drug development, medical devices, and healthcare technology offer exceptional growth potential — particularly for companies with proprietary treatments for large, underserved patient populations. Patent protection provides explicit regulatory moats. The risks are real: drug development failure rates are high, regulatory approval is uncertain, and pricing pressure from governments and insurers is a persistent headwind. But blockbuster drugs or medical devices can generate decades of protected high-margin revenue.

Consumer Discretionary

Exceptional consumer brands and retail concepts can compound for decades by expanding geographically, extending product lines, and deepening customer loyalty. Starbucks, Nike, and Lululemon each grew from niche concepts to global brands through consistent execution over decades. Consumer growth companies benefit from the emotional and habitual nature of brand loyalty — once customers are attached, they’re remarkably sticky.

Financial Technology

The digitization of financial services — payments, lending, wealth management, insurance — is an ongoing multi-decade growth trend as traditional financial infrastructure shifts to software-based models. Companies like Visa, Mastercard, PayPal, and Square (Block) have grown by capturing a small percentage of massive transaction volumes with highly scalable software infrastructure.

📉 When to Sell a Growth Stock

Many growth investors focus almost exclusively on when to buy — and then struggle with the harder question of when to sell. These are the clearest signals that it’s time to reassess or exit a growth position:

The thesis has changed: You bought because of specific growth drivers (new product category, geographic expansion, market share gains). If those drivers are no longer materializing — competition won, the product failed, the market didn’t develop as expected — the original reason for owning the stock is gone regardless of current price.

Growth is structurally decelerating beyond expectations: Every company eventually grows more slowly. If a company’s growth is decelerating faster than the market has priced in, the stock remains overvalued even after significant price declines. Revenue growth dropping from 40% to 15% to 8% over three years is a structural shift, not a temporary hiccup.

Valuation has become extreme: When a stock’s price has risen so far ahead of business fundamentals that even excellent execution can’t justify the valuation, the risk-reward has deteriorated. Selling a portion of an excellent business at extreme valuations and redeploying into better risk-adjusted opportunities is rational portfolio management.

Better opportunities exist: The cost of holding a mediocre position is not just the returns lost — it’s the better position you could have held instead. When you identify a demonstrably better risk-adjusted opportunity, owning your current position purely out of inertia is a mistake.

Position size has become dangerous: A growth stock that has performed extraordinarily well may now represent 30–40% of your portfolio. The concentration risk of this position — regardless of business quality — can make your financial outcomes dependent on one company’s continued success. Trimming to a more manageable position size is risk management, not pessimism.

For a complete toolkit covering when to buy, hold, and sell stocks across all strategies, read our guides on stock investment strategies, how to read stock charts for timing signals, and how to find the best stocks to invest in for building your initial candidate list.

To complete the P3 strategy group, see our guide on dividend investing — a strategy focused on building reliable passive income through companies that pay and grow their dividends consistently.