What if the best investment strategy in the world required zero skill, zero market knowledge, and only 10 minutes to set up — then ran on autopilot forever? That strategy exists. It’s called dollar-cost averaging. And the fact that it consistently outperforms most active traders isn’t a secret — it’s just widely ignored.

This guide explains exactly what dollar-cost averaging is, the math that makes it work, when it beats lump-sum investing, when it doesn’t, and how to implement it in a way that actually compounds wealth over decades — not just sounds good in theory.

💡 What Is Dollar-Cost Averaging?

Dollar-cost averaging (DCA) is an investment strategy where you invest a fixed dollar amount at regular intervals — weekly, monthly, quarterly — regardless of what the market is doing.

You don’t wait for the “right moment.” You don’t try to buy dips or avoid peaks. You invest your $200 (or $500, or $2,000) on the same schedule, every period, rain or shine, bull market or crash. The amount is fixed. The schedule is fixed. The execution is automatic.

What changes is how many shares you get. When prices are low, your fixed amount buys more shares. When prices are high, it buys fewer. Over time, this natural mechanism means your average cost per share trends below the market’s average price — which is the mathematical edge that makes DCA so powerful for long-term investors.

🧮 The Math That Makes DCA Work

The core insight behind DCA is a mathematical property called the harmonic mean. When you invest a fixed dollar amount at varying prices, your average cost per share is always lower than the simple average of the prices you paid at.

Here’s a concrete example. Imagine investing $300/month in an ETF over 4 months at these prices:

- Month 1: Price = $50 → $300 buys 6.0 shares

- Month 2: Price = $40 → $300 buys 7.5 shares

- Month 3: Price = $30 → $300 buys 10.0 shares

- Month 4: Price = $60 → $300 buys 5.0 shares

Total invested: $1,200. Total shares: 28.5. Your actual average cost per share: $1,200 ÷ 28.5 = $42.11

Simple average of the four prices: ($50 + $40 + $30 + $60) ÷ 4 = $45.00

Your DCA cost ($42.11) is $2.89 lower per share than the simple average. On 28.5 shares, that’s $82 in extra value — from the math alone, with no skill required.

This isn’t luck. It’s structural. Because you invested more dollars when prices were low (Month 3: 10 shares for $300) and fewer dollars when prices were high (Month 4: 5 shares for $300), your portfolio naturally accumulates more shares at lower prices.

📅 Why Regular Investing Beats Market Timing

The alternative to DCA is trying to time the market — waiting until prices look “right” before investing. This sounds logical. In practice, it fails consistently.

The data is unambiguous:

- A 2020 Schwab study found that even the worst possible market timer — someone who invested their lump sum at the highest point of every year — still dramatically outperformed someone who never invested and kept cash

- Missing just the 10 best trading days in the S&P 500 over a 20-year period reduced returns by more than half

- Those 10 best days almost always occur during or immediately after the worst crashes — exactly when market timers are on the sidelines

The fundamental problem with market timing: it requires being right twice — when to get out AND when to get back in. Professional fund managers with entire research teams and real-time data fail at this consistently. Individual investors, operating on emotion and part-time attention, fail even more reliably.

DCA sidesteps the entire problem. You’re not trying to predict markets. You’re systematically accumulating ownership in great companies regardless of short-term price movements. Time in the market beats timing the market — and DCA is the mechanism that keeps you in the market, always.

🐻 DCA’s Superpower: Market Crashes Become Your Friend

This is the most counterintuitive — and most powerful — aspect of dollar-cost averaging.

When the market crashes 30% and your portfolio value drops, most investors panic. But for a committed DCA investor, a crash is a sale event. Your fixed monthly investment now buys significantly more shares at cheaper prices. The lower the price falls, the more ownership you accumulate with each contribution.

Consider two investors, both putting $500/month into a broad market ETF:

Investor A (Panic seller): Market crashes 40%. Stops contributions. Waits for recovery. Misses the bottom. Resumes investing after prices have recovered 50%. Bought almost nothing at the lows.

Investor B (DCA disciplined): Market crashes 40%. Continues $500/month contributions without change. Accumulates 67% more shares at the bottom compared to pre-crash prices. When market recovers, each of those cheap shares contributes to larger gains.

The 2008–2009 financial crisis illustrated this perfectly. Investors who kept contributing through the bottom of March 2009 accumulated massive positions in the best companies at their lowest prices in years. The subsequent decade-long bull market multiplied those positions enormously. The investors who stopped contributing missed the most valuable accumulation window in a generation.

Volatility — which most investors fear — is the mechanism that makes DCA work. Without price fluctuation, the harmonic mean advantage disappears. Paradoxically, more volatile markets often produce better DCA outcomes for patient, disciplined investors than smooth upward trends do.

💰 DCA vs. Lump-Sum Investing: The Honest Comparison

Here’s where intellectual honesty matters. DCA isn’t always mathematically optimal — and understanding when it is and isn’t changes how you use it.

When Lump-Sum Beats DCA

Multiple studies — including research from Vanguard — have found that in approximately two-thirds of historical periods, investing a lump sum immediately outperforms spreading that same money through DCA over 12 months. The reason: markets go up more often than they go down. If you have $12,000 to invest and markets rise 15% over the next year, the $12,000 invested immediately grows more than $1,000/month invested throughout the year.

If you have a large amount of cash available right now and a long time horizon, the mathematically optimal strategy is often to invest it all immediately.

When DCA Wins

DCA genuinely wins in these circumstances:

- You don’t have a lump sum: You earn income monthly and invest as you earn. DCA isn’t a choice — it’s the only practical option. For most working people, this is the reality.

- Volatile or declining markets: When markets are falling or highly volatile, DCA systematically accumulates more shares at lower prices, often producing better outcomes than a lump sum invested before the decline.

- Psychological sustainability: The “mathematically optimal” strategy that causes you to panic-sell during a crash produces terrible real-world returns. DCA’s smaller, regular contributions reduce the psychological weight of each investment decision — making it far easier to stay disciplined through turbulence. A strategy you can actually stick to beats an optimal strategy you’ll abandon under pressure.

- Uncertain timing: If you’re worried markets are overvalued but still want to invest, DCA lets you participate while reducing the risk of a single large purchase at a market peak.

The Bottom Line

For most people with regular income who invest monthly, DCA isn’t a choice between strategies — it’s simply the practical implementation of investing consistently. The academic debate about lump sum vs. DCA matters primarily for people who receive windfalls (inheritance, bonus, asset sale proceeds). For everyone else: automate monthly investments and focus on contribution amount and asset allocation rather than timing.

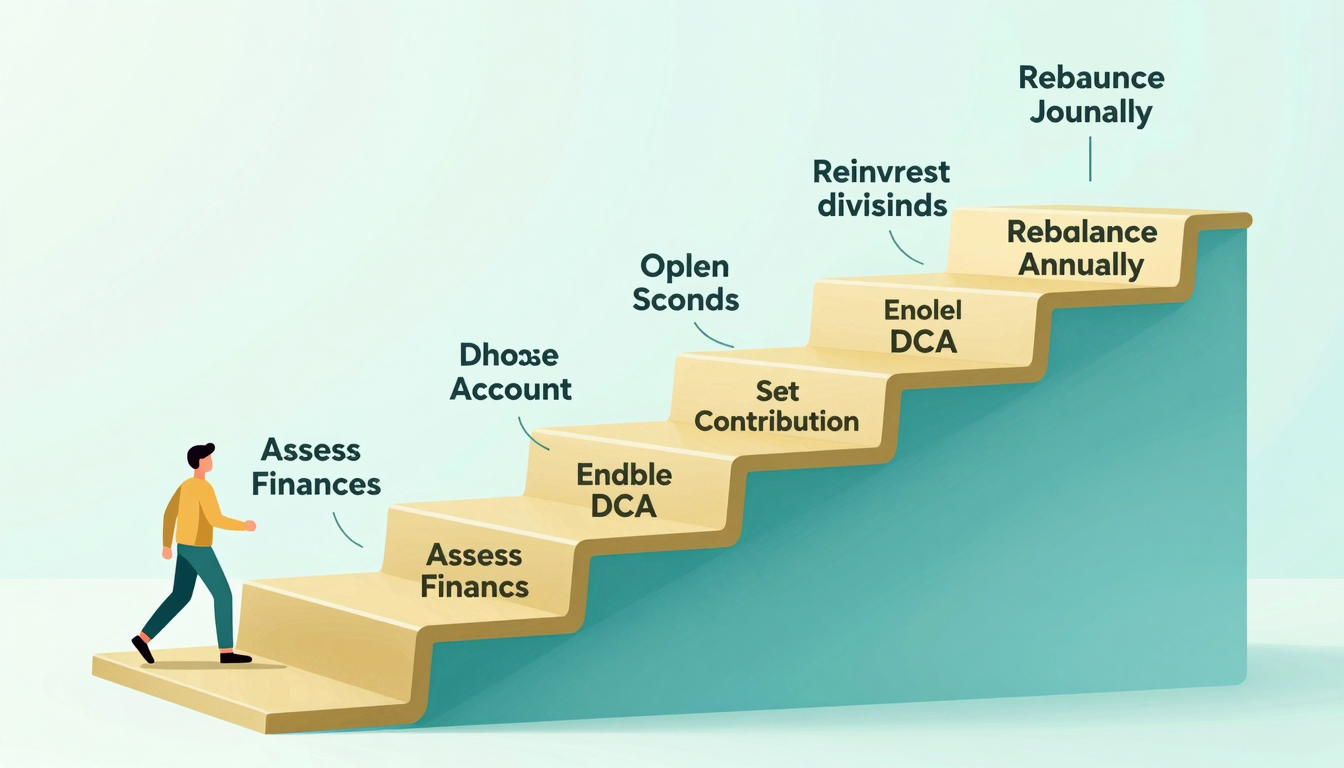

⚙️ How to Set Up Dollar-Cost Averaging (Step by Step)

The tactical setup is straightforward. Here’s exactly how to implement DCA:

Step 1: Choose Your Investment Vehicle

DCA works best with broad, diversified, liquid investments:

- 🌍 Broad market ETFs: VTI (total US market), VOO (S&P 500), VT (total world market) — instant diversification, low costs, perfectly suited for DCA

- 🏦 Index mutual funds: Same concept as ETFs, sometimes with automatic investment features built in at the fund level

- 🎯 Target-date funds: All-in-one funds that automatically adjust stock/bond allocation as you approach a target retirement date

Avoid using DCA on individual stocks unless you have high conviction and a robust understanding of the company. The diversification of broad ETFs makes DCA far more effective — a single company can fail permanently; the broad market never has.

Step 2: Determine Your Contribution Amount

This is more important than which ETF you choose. Set an amount that:

- You can consistently contribute without financial stress in any month

- Leaves your emergency fund (3–6 months expenses) intact and untouched

- Reflects an amount you can increase annually as your income grows

Starting with $100/month consistently beats starting with $500/month inconsistently. The discipline matters more than the initial amount.

Step 3: Choose Your Interval

Monthly is the most common and practical schedule for most investors — aligning with paycheck cycles and eliminating decision fatigue. Weekly contributions provide slightly better mathematical DCA benefit (more price points, smoother averaging) but at the cost of more transactions and complexity. Biweekly (every two weeks, aligned to paychecks) is an excellent compromise.

Step 4: Automate Everything

This is non-negotiable. Set up automatic investments through your brokerage:

- Fidelity: Automatic Investments feature → select ETF → set dollar amount → choose frequency

- Schwab: Automatic Investing → configure recurring purchases

- Vanguard: Automatic Investment Plan → available for Vanguard funds

Once automated, the investment happens without any action from you. You don’t need to log in. You don’t need to think about it. You don’t need willpower during market crashes. The system executes regardless of headlines, emotions, or market conditions.

Step 5: Revisit Annually

Once per year: review your contribution amount and increase it if your income has grown. Rebalance your portfolio back to target allocations if significant drift has occurred. Beyond that annual review, the optimal DCA approach is benign neglect — set it and let compounding do the work.

🏛️ DCA Inside Tax-Advantaged Accounts

Dollar-cost averaging is most powerful when implemented inside tax-advantaged accounts:

401(k) contributions: If you contribute a percentage of each paycheck to your 401(k), you’re already DCA-ing automatically. Your contribution goes in each payday regardless of market conditions. This is one of the best financial behaviors you can establish — and most people already have it set up without realizing it’s a deliberate investment strategy.

Roth IRA: $7,000 annual contribution limit (2024). Spreading contributions monthly ($583/month) rather than depositing the full $7,000 in January implements DCA and avoids timing risk. Contributions grow completely tax-free — DCA’s compounding advantage is amplified without tax drag on gains.

Traditional IRA: Same contribution limits as Roth IRA. Tax deduction on contributions (subject to income limits). Same DCA implementation applies.

The combination of DCA’s mechanical advantage, tax-free compounding inside retirement accounts, and the behavioral benefit of automation creates one of the most reliable wealth-building systems available to individual investors. For a complete guide to how stock investing fits into long-term wealth building, see our pillar resource on what stock investment really means.

🧠 The Psychology of DCA: Why It Works When Nothing Else Does

Finance theory often ignores human psychology. DCA accounts for it explicitly — and that’s a large part of why it works in the real world when theoretically superior strategies fail in practice.

Decision fatigue elimination: Every investment decision is a cognitive load. DCA reduces hundreds of individual decisions to one setup decision that governs all future contributions. Your mental bandwidth is freed for other things.

Emotional detachment from short-term prices: Once you automate DCA, day-to-day or month-to-month market movements become irrelevant to your process. The check goes in on schedule. You stop obsessing over whether “now is a good time” — because you’ve pre-decided that every time is a good time within your long-term strategy.

Reduced regret risk: The most paralyzing investment fear is deploying a large sum and watching it immediately fall 20%. DCA spreads this risk across many smaller decisions. If the market drops 20% after your monthly contribution, you’ve lost on one month’s amount — not your entire available capital.

Behavioral alignment with reality: Most people don’t receive lump sums — they earn regular income. DCA matches investment behavior to income timing, making it the natural, sustainable approach for the vast majority of investors throughout their working lives.

❓ Frequently Asked Questions

Can I DCA with any amount?

Yes. Fractional shares (available at Fidelity, Schwab, Robinhood, and others) let you invest any dollar amount — $25, $50, $100 — in any stock or ETF regardless of the share price. There’s no practical minimum for DCA with a modern brokerage account.

Should I DCA into individual stocks or ETFs?

ETFs are far better suited for DCA. A broad market ETF like VTI represents thousands of companies — if any individual company within the ETF fails, your portfolio barely flinches. DCA into a single company stock works fine if you have high conviction, but you’re concentrating risk in a way that ETF DCA eliminates. For most investors: DCA into broad ETFs for the core portfolio, with individual stock exposure (if desired) limited to a smaller satellite allocation.

What if I miss a month?

Life happens. Missing one or two monthly contributions has negligible long-term impact. The important thing is resuming immediately. Don’t try to “make up” missed contributions by investing a larger lump sum — that reintroduces timing risk. Just return to your regular schedule and continue.

Should I stop DCA during a market crash?

The opposite — continue DCA through market crashes, and consider temporarily increasing contributions if your financial situation allows. Crashes are the periods when DCA accumulates the most shares at the lowest prices. Stopping contributions during downturns eliminates DCA’s primary benefit and locks in the worst possible outcome: high average cost, low share count.

How is DCA different from a savings plan?

A savings plan deposits money into a cash account (savings, money market) where it earns fixed interest. DCA invests in market assets (stocks, ETFs) that carry risk but provide significantly higher expected long-term returns. DCA involves real investment risk — your balance fluctuates with market prices. Unlike savings, DCA positions aren’t FDIC-insured and can lose value. The trade-off: historical long-term returns from DCA into broad stock ETFs have dramatically exceeded savings account returns over any 10+ year period.

✅ Key Takeaways

- 🔹 DCA = fixed dollar amount invested at regular intervals, regardless of market conditions

- 🔹 The harmonic mean math ensures your average cost per share is always below the average price — a structural, skill-free advantage

- 🔹 Market crashes become accumulation opportunities, not disasters — DCA buys more shares when prices are low

- 🔹 Lump-sum investing is theoretically optimal when markets rise — but DCA wins on psychology, practicality, and volatile markets

- 🔹 Automate contributions so execution doesn’t require willpower

- 🔹 Works best in broad market ETFs inside tax-advantaged accounts

- 🔹 Annual review of contribution amount is the only active management required

- 🔹 The best DCA investor is a boring one — consistent, automatic, emotionally detached from short-term noise

The most powerful wealth-building strategies are almost always the simplest. Dollar-cost averaging requires no market expertise, no prediction, no perfect timing. Just consistency, automation, and time. Those three ingredients, combined with broad market exposure, have built more middle-class wealth than any other investment approach in history.

📊 Real-World DCA Scenarios: What the Numbers Look Like

Theory is convincing. Numbers are more convincing. Here’s what consistent DCA actually produces over different time horizons, assuming an average annual return of 8% (conservative estimate for a broad US stock market ETF after inflation adjustment):

$200/Month for 10 Years

Total contributions: $24,000. Portfolio value at 8% average annual return: approximately $36,590. That’s $12,590 in investment gains — more than 50% above your total contributions — generated entirely through consistent monthly investing with zero active management.

$200/Month for 20 Years

Total contributions: $48,000. Portfolio value: approximately $117,804. Your $48,000 became nearly $118,000 — nearly 2.5x your contributions — through compounding alone. The last decade contributed far more growth than the first, demonstrating why time is the most powerful variable in the equation.

$200/Month for 30 Years

Total contributions: $72,000. Portfolio value: approximately $298,072. Nearly $300,000 from $200/month. The compounding in years 20–30 generated more wealth than the previous 20 years combined. This is why starting early — even with modest amounts — matters far more than investing larger amounts later.

Increasing Contributions Over Time

The most realistic and powerful approach: increase your monthly DCA contribution each year as your income grows. Starting at $200/month and increasing by $50/year over 30 years (reaching $1,650/month by year 30) would produce dramatically higher outcomes — well into the $600,000–$800,000 range at 8% average returns. The combination of DCA discipline, annual contribution increases, and compound growth is the foundation of how ordinary earners build extraordinary wealth.

🔗 DCA as Part of Your Complete Investment Strategy

Dollar-cost averaging isn’t an investment strategy on its own — it’s a contribution methodology. It answers “when and how often to invest” but doesn’t answer “what to invest in” or “how much risk to take.”

The complete picture requires combining DCA with:

- Asset allocation: The ratio of stocks to bonds to other assets based on your timeline and risk tolerance

- Diversification: Spreading investments across market segments, sectors, and geographies

- Tax optimization: Maximizing tax-advantaged account contributions before taxable accounts

- Annual rebalancing: Returning to target allocations when markets drift your portfolio away from them

When DCA combines with a well-diversified portfolio of low-cost index ETFs inside tax-advantaged accounts, reviewed and rebalanced annually, the result is one of the most powerful and reliable wealth-building systems available to individual investors — requiring minimal expertise and minimal active management time.

To understand the full investment approach that DCA supports, read our comprehensive guides on stock investment strategies, how to invest in stocks step by step, and everything beginners need to know about the stock market.

🌍 DCA Around the World: Different Markets, Same Principle

Dollar-cost averaging is a universal principle — it works in any liquid market, in any currency, in any country. US investors have the most platform options and the lowest-cost ETFs, but the strategy applies globally.

European investors: Many European brokers and fintech platforms (Scalable Capital, Trade Republic, DEGIRO) offer automatic investment plans into UCITS ETFs — the European equivalent of US ETFs. The same DCA mechanics apply. Look for iShares, Vanguard, and Amundi UCITS ETFs tracking broad global or regional indices.

Asian investors: Emerging and developed Asian markets have seen significant fintech growth enabling regular investment plans. Singapore’s brokerage platforms, Hong Kong’s stock connect access to mainland China, and Japan’s NISA tax-advantaged accounts all support DCA-style regular investing into broad market indices.

Emerging market investors: Currency risk adds complexity for investors in high-inflation environments. Investing in US-dollar-denominated ETFs through international brokers like IBKR provides both market exposure and implicit currency diversification — though local currency fluctuations can significantly affect real returns. Consider this dimension when applying DCA principles to cross-border investing.

The core principle — consistent, automatic, schedule-driven investment regardless of market conditions — produces its mathematical advantage in any liquid market. The specific implementation details vary by country, brokerage, and tax regime; the underlying logic remains constant.

⚠️ Common DCA Mistakes to Avoid

Mistake 1: Treating DCA as a Reason to Ignore Asset Allocation

DCA tells you how often to invest, not what to invest in. Consistently DCA-ing into a poorly diversified or inappropriate portfolio doesn’t fix bad asset allocation. Get your investment selection right first, then automate contributions through DCA.

Mistake 2: Stopping During Volatility

The entire value of DCA comes from maintaining contributions through market downturns — when you accumulate the most shares at the lowest prices. Stopping contributions during crashes converts DCA from wealth-building discipline to a strategy that buys high and pauses during lows. This is the opposite of the intended effect.

Mistake 3: Setting a Fixed Amount and Never Increasing It

A $200/month DCA contribution in year 1 should not still be $200/month in year 10 if your income has grown significantly. Failing to increase contributions as your earnings grow leaves substantial wealth-building potential on the table. Set a calendar reminder to review and increase your contribution amount annually.

Mistake 4: Using DCA for Short-Term Goals

DCA is a long-term strategy. Investing in volatile assets (stocks, ETFs) through DCA for money you’ll need in 1–3 years exposes that capital to sequence-of-returns risk — if markets crash right before you need the money, you may have to sell at a loss. Short-term goals belong in stable, liquid vehicles: high-yield savings accounts, short-term CDs, or money market funds.

Mistake 5: Confusing DCA with Active Trading

DCA is a passive, systematic strategy. Its power comes from removing active decision-making. Some investors set up monthly DCA plans but then override the automation — buying extra when markets seem cheap, pausing when markets seem high. This defeats the purpose. Trust the system. The automation is the strategy.