When someone says “the market was up 1.2% today,” they’re not describing all 6,000+ publicly traded U.S. companies. They’re describing a single number: a stock market index.

Indexes are the scoreboard of capitalism. They compress the collective performance of dozens, hundreds, or thousands of companies into a single data point that tells investors — at a glance — how markets are moving. Understanding what indexes are, how they’re built, and why they matter transforms how you interpret financial news and make investment decisions.

What Is a Stock Market Index?

A stock market index is a statistical measure that tracks the performance of a selected group of stocks, representing a specific market segment, sector, country, or investment style.

The index itself is not an investment — it’s a benchmark. You can’t buy “the S&P 500” directly. But you can buy funds that track it — which is where index investing becomes one of the most powerful strategies available to ordinary investors.

The three functions of market indexes:

Benchmarking — Measuring portfolio performance against a standard (“Did I beat the market?”)

Market temperature — Providing a quick read on overall market sentiment and direction

Investment vehicle — Serving as the basis for index funds and ETFs that anyone can buy

The Major U.S. Stock Market Indexes

Index

Founded

Components

Weighting Method

What It Represents

S&P 500

1957

500 companies

Market-cap weighted

Large-cap U.S. stocks; the most widely followed benchmark

Dow Jones Industrial Average

1896

30 companies

Price-weighted

30 blue-chip U.S. companies; oldest major index

Nasdaq Composite

1971

3,000+ companies

Market-cap weighted

All Nasdaq-listed stocks; heavy technology weighting

Nasdaq-100

1985

100 companies

Market-cap weighted

100 largest non-financial Nasdaq companies; the “tech index”

Russell 2000

1984

2,000 companies

Market-cap weighted

Small-cap U.S. stocks; indicator of domestic economy health

Russell 3000

1984

3,000 companies

Market-cap weighted

~96% of all investable U.S. stocks by market cap

Wilshire 5000

1974

~3,400 companies

Market-cap weighted

Broadest U.S. equity index; “total market”

How Indexes Are Calculated: The 3 Weighting Methods

Not all indexes are built the same way. The weighting methodology determines how much influence each component stock has on the overall index level — and has significant implications for how the index behaves.

1. Market-Cap Weighting (Most Common)

Used by: S&P 500, Nasdaq, Russell indexes, MSCI indexes

Each stock’s weight in the index is proportional to its market capitalization (share price × shares outstanding). The largest companies have the most influence.

Example — S&P 500: Apple, Microsoft, Nvidia, Amazon, and Alphabet collectively represent roughly 25–30% of the entire index. A 5% move in Apple moves the S&P 500 more than a 50% move in a small component.

Advantage: Naturally reflects economic reality — larger companies deserve more weight because they represent more of the economy’s total value.

Disadvantage: Concentration risk. When large-cap technology stocks are extremely expensive relative to fundamentals, the entire index carries that valuation risk disproportionately.

2. Price Weighting (Historical Method)

Used by: Dow Jones Industrial Average

Each stock’s weight is determined solely by its share price — not its market cap. A $300 stock has three times the influence of a $100 stock, regardless of company size.

Example — DJIA: UnitedHealth Group (priced at ~$500+) has more index weight than Apple (priced at ~$180), even though Apple’s market cap is several times larger.

Why it’s outdated: Share price alone is arbitrary — companies can split their stock to lower price or do reverse splits to raise it. Price weighting creates distortions that market-cap weighting avoids. The DJIA persists primarily because of its 125+ year history and brand recognition, not methodological superiority.

3. Equal Weighting

Used by: RSP (Invesco S&P 500 Equal Weight ETF) and specialty indexes

Every component receives an identical weight regardless of market cap or price. In an equal-weighted S&P 500, each of the 500 stocks represents 0.2% of the index.

Advantage: More exposure to smaller companies within the index; historically outperforms market-cap weighted over very long periods (value tilt).

Disadvantage: Higher turnover (requires frequent rebalancing), higher costs, and underperforms when large-caps are driving market gains (as in 2023–2024).

Key Global Stock Market Indexes

Index

Country/Region

Components

Key Feature

FTSE 100

United Kingdom

100 companies

London Stock Exchange’s largest companies

DAX 40

Germany

40 companies

Germany’s largest listed companies; total return index

Nikkei 225

Japan

225 companies

Japan’s most watched index; price-weighted

Hang Seng

Hong Kong

80 companies

HK’s benchmark; includes mainland Chinese listings

CSI 300

China

300 companies

Top 300 stocks on Shanghai + Shenzhen exchanges

MSCI World

Global (Developed)

1,500+ companies

23 developed market countries; global benchmark

MSCI Emerging Markets

Global (Emerging)

1,400+ companies

24 emerging market countries including China, India, Brazil

Why Index Funds Beat Most Active Managers

The most important practical implication of understanding indexes: you can invest in them directly through index funds — and doing so outperforms the vast majority of professional fund managers over the long term.

The S&P 500 has returned approximately 10% annually on average over the last century. The percentage of actively managed large-cap funds that beat the S&P 500 over 15-year periods: roughly 10–15%. The other 85–90% underperform — and that’s before accounting for taxes on higher turnover.

Why it’s so hard to beat an index:

Cost drag — Active funds charge 0.5–1.5% annually; index funds charge 0.03–0.10%. That gap compounds enormously over decades.

Information efficiency — Modern markets incorporate publicly available information quickly. Consistent edges based on public data are rare.

Behavioral drag — Active managers face pressure to “do something” during volatile markets. Index funds have no such pressure — they simply hold.

Survivorship bias — Underperforming funds are closed or merged, making the published track record of “active management” look better than reality.

How to Invest in an Index

You invest in an index through index funds or ETFs that track it. Both hold the same underlying stocks in the same proportions as the index — the difference is structural:

Feature

Index Mutual Fund

Index ETF

Trading

Once per day at NAV

Intraday, like a stock

Minimum investment

Often $1–$3,000

Price of one share (or fractional)

Tax efficiency

Good

Slightly better (in-kind redemptions)

Expense ratio

0.03–0.15%

0.03–0.20%

Best for

Automatic monthly investing

Flexible buying/selling, taxable accounts

Most popular index funds/ETFs by index:

S&P 500: VOO, IVV, FXAIX, SPY

Total US Market: VTI, FSKAX, SWTSX

Nasdaq-100: QQQ, QQQM

Total World: VT, FWWFX

International Developed: VEA, FSPSX

Emerging Markets: VWO, FPADX

Reading an Index: What the Numbers Actually Mean

The raw number of an index (S&P 500 at 5,300, for example) is meaningless in isolation — it’s an arbitrary starting value scaled over time. What matters is:

Percentage change: “The S&P 500 is up 1.2%” is meaningful. “The S&P 500 is at 5,342” alone is not.

Year-to-date return: How the index has performed since January 1st of the current year.

Trailing 1/3/5/10-year returns: Long-term context that smooths out short-term volatility.

P/E ratio of the index: The aggregate valuation of all components — useful for assessing whether the overall market is cheap or expensive relative to history.

Sector Indexes: A Layer Deeper

Within broad indexes, sector indexes track specific industries. The S&P 500, for example, is divided into 11 GICS (Global Industry Classification Standard) sectors, each with its own index and corresponding ETF:

Sector

ETF

S&P 500 Weight (~)

Information Technology

XLK

~32%

Healthcare

XLV

~12%

Financials

XLF

~13%

Consumer Discretionary

XLY

~10%

Communication Services

XLC

~9%

Industrials

XLI

~8%

Consumer Staples

XLP

~6%

Energy

XLE

~4%

Utilities

XLU

~2%

Real Estate

XLRE

~2%

Materials

XLB

~2%

Sector ETFs let investors tilt their portfolio toward sectors they believe will outperform without abandoning diversification entirely.

Common Questions About Stock Market Indexes

Which index is the best to invest in?

For most investors, a total market index (VTI, FSKAX) or S&P 500 index (VOO, FXAIX) is the optimal starting point. Total market funds provide broader diversification including small and mid-cap stocks. S&P 500 funds focus on the largest, most established companies. Over long periods, their returns are very similar.

What’s the difference between the S&P 500 and the Dow Jones?

The S&P 500 contains 500 companies weighted by market capitalization — it’s a far more comprehensive and methodologically sound measure of the US large-cap market. The Dow contains only 30 companies and uses an outdated price-weighting method. Most professional investors use the S&P 500 as their primary US market benchmark.

Can an index go to zero?

The S&P 500 going to zero would require all 500 companies in it to simultaneously become worthless — which would mean the effective collapse of the U.S. economy. This is theoretically possible but practically equivalent to a scenario where money itself has lost meaning. For any investment horizon measured in years or decades, this risk is not meaningfully distinguishable from zero.

How often is an index rebalanced?

The S&P 500 is rebalanced quarterly, with component changes announced in advance. A company can be added (typically when it meets size, liquidity, and profitability criteria) or removed (due to mergers, delistings, or falling below eligibility thresholds). Index funds automatically adjust to reflect these changes.

Is the stock market index the same as the economy?

No — and this distinction matters. Stock market indexes reflect the collective earnings expectations and valuation of listed public companies, which can diverge significantly from the broader economy (GDP growth, unemployment, etc.). In 2020, stocks recovered to all-time highs while millions remained unemployed. Markets are forward-looking and often disconnect from current economic conditions.

The hardest part of investing isn’t picking the right stocks or timing the market. It’s starting. Every year you delay costs you years of compounding — and compounding, over time, is the most powerful wealth-building force available to ordinary people.

This guide is a pure action plan. No theory for theory’s sake, no academic detours. Just seven concrete steps that take you from zero to making your first investment — with the right foundation to keep going for decades.

Step 1: Build Your Emergency Fund First

Before investing a single dollar in the stock market, you need 3–6 months of living expenses in a high-yield savings account. This isn’t optional — it’s the foundation everything else rests on.

Why this comes first: The stock market can decline 30–50% in any given year. If you invest without an emergency fund and a crisis hits (job loss, medical bill, car repair), you may be forced to sell investments at the worst possible time — locking in losses instead of riding through the recovery.

Where to keep it: High-yield savings accounts (HYSAs) currently offer 4–5% APY — meaningfully above traditional savings accounts. Your emergency fund should be liquid and accessible, not invested in stocks.

Target amount:

Situation

Recommended Emergency Fund

Stable job, low fixed expenses

3 months of expenses

Variable income (freelance, sales)

6 months of expenses

Single income household

6+ months of expenses

With dependents or health issues

6–12 months of expenses

Step 2: Clear High-Interest Debt

Credit card debt at 20–25% APR is a guaranteed 20–25% return when you pay it off — better than any stock market investment can reliably deliver. Paying down high-interest debt is the highest-return, zero-risk “investment” available.

The threshold: Pay off any debt with an interest rate above ~6–7% before investing. Below that threshold, the expected long-term stock market return (~7–10% historically) may exceed the guaranteed return of paying down debt — but this depends on your risk tolerance.

Student loans and mortgages at lower rates (3–5%) can generally be maintained while investing simultaneously — the math often favors investing while making minimum payments on low-rate debt.

Step 3: Understand Your Account Options

Where you invest matters almost as much as what you invest in. Tax-advantaged accounts can significantly improve long-term outcomes.

Account Type

Tax Benefit

2024 Contribution Limit

Best For

401(k) / 403(b)

Pre-tax contributions; tax-deferred growth

$23,000 ($30,500 if 50+)

Employer-sponsored; especially valuable with employer match

Roth IRA

After-tax contributions; tax-FREE growth and withdrawals

$7,000 ($8,000 if 50+)

Best for those expecting to be in higher tax bracket at retirement

No tax advantage; but no contribution limits or restrictions

Unlimited

After maxing tax-advantaged accounts, or for shorter-term goals

HSA

Triple tax advantage: pre-tax in, tax-free growth, tax-free medical withdrawals

$4,150 individual / $8,300 family

Must have high-deductible health plan; exceptional for healthcare costs

The optimal order for most people:

401(k) up to employer match (free money — always do this first)

HSA if eligible (triple tax advantage)

Roth IRA up to annual limit

401(k) up to annual limit

Taxable brokerage account (unlimited)

Step 4: Choose a Brokerage

The brokerage landscape has converged dramatically — almost all major brokers now offer $0 commissions, fractional shares, and excellent mobile apps. The differences are marginal for most investors.

For beginners, prioritize:

No account minimums — Start with any amount

Fractional shares — Buy $50 of a $500 stock

Clean interface — You’ll use this for decades; it should feel intuitive

Educational resources — Good brokers invest in helping their users learn

Well-regarded options: Fidelity (top-rated for beginners, excellent research), Schwab (strong all-around, great customer service), Vanguard (ideal for long-term index fund investors), and others. For a complete walkthrough of opening your first account, see our guide on how to open a brokerage account.

Step 5: Make Your First Investment

For most beginning investors, the right first investment is not an individual stock — it’s a broad market index fund.

Why index funds first:

Instant diversification across hundreds or thousands of companies

Ultra-low costs (expense ratios as low as 0.03%)

Outperforms the majority of actively managed funds over 10+ years

No research required — you own the entire market

Removes the risk of picking a single stock that underperforms

Three starting points for most investors:

Fund

What It Owns

Expense Ratio

Ticker

Total US Market Index

~3,500+ US stocks, all cap sizes

0.03%

VTI (Vanguard), FSKAX (Fidelity)

S&P 500 Index

500 largest US companies

0.03%

VOO (Vanguard), FXAIX (Fidelity), IVV (iShares)

Total World Index

US + international stocks

0.07%

VT (Vanguard), FWWFX (Fidelity)

If you want to invest in individual stocks instead — or in addition to index funds — our guides on how to pick stocks and best stocks to invest in cover the full methodology.

Step 6: Set Up Automatic Contributions

The single most powerful thing you can do after making your first investment: automate it.

Set a recurring transfer — weekly, bi-weekly, or monthly — from your checking account to your investment account. Then set the investment account to automatically invest that contribution in your chosen fund.

Why automation beats manual investing:

Removes behavioral friction — you never have to “decide” to invest

Forces dollar-cost averaging automatically — you buy more when prices are low, less when they’re high

Removes the temptation to time the market — the decision is already made

Builds investing as a habit rather than an occasional action

Even $100/month invested consistently from age 25 grows to approximately $350,000 by age 65 at a 7% average annual return — without ever increasing contributions. Increasing that amount over time as income grows produces dramatically larger outcomes.

For the full framework on automated investing and its compounding power, see our guide on dollar-cost averaging.

Step 7: Build Your Knowledge Over Time

Starting with index funds doesn’t mean staying there forever. As you invest consistently and build confidence, you may want to:

Add individual stocks alongside your core index fund holdings

Diversify into bonds or international stocks as your portfolio grows

Develop a deeper understanding of valuation and company analysis

Optimize for tax efficiency as your income and portfolio grow

The key is building knowledge progressively — not trying to master everything before starting. Start simple, start now, and add complexity only as it’s warranted by your portfolio size and confidence level.

The Investing Roadmap: Where You Are and Where You’re Going

Stage

Portfolio Size

Focus

Key Actions

Foundation

$0 – $10K

Habit formation, tax setup

Emergency fund, open IRA/401k, first index fund, automate

Accumulation

$10K – $100K

Consistency, diversification

Max tax-advantaged accounts, add sector diversity, begin reading

Growth

$100K – $500K

Optimization, individual stocks

Taxable brokerage, stock picking if desired, rebalancing discipline

Wealth Building

$500K+

Tax efficiency, income

Estate planning, tax-loss harvesting, dividend income optimization

Common Beginner Mistakes to Avoid

Waiting for the “Right Time”

There is no right time. Markets are at all-time highs roughly 30% of the time — buying at all-time highs and holding for 10+ years has historically produced positive returns. The cost of waiting is paid in compounding years lost.

Checking Your Portfolio Daily

Daily price checking is the fastest path to bad decisions. Stock prices fluctuate constantly for reasons that have nothing to do with the underlying business. Check your portfolio quarterly at most — monthly if you’re disciplined. Never trade based on daily movements.

Investing Money You’ll Need Soon

The stock market is for money you won’t need for at least 3–5 years. Shorter time horizons belong in savings accounts or short-term bonds. Markets can and do fall 30–50% — you need time to ride out downturns without being forced to sell.

Chasing Last Year’s Winners

The funds and sectors that performed best last year are often the worst performers the next year. Sector rotation is real. Buy based on valuation and fundamentals, not recent momentum.

Trying to Pick the Bottom

Nobody consistently picks market bottoms. Investors who wait for “a better price” during a decline often miss the recovery entirely — and the best days in markets frequently come immediately after the worst days.

Common Questions About Starting to Invest

How much money do I need to start investing?

Most major brokers now have no account minimums. With fractional shares, you can invest as little as $1. The “right” amount to start is whatever you can consistently commit to — even $50 per month builds meaningful wealth over decades through compounding.

Is now a good time to start investing?

For long-term investors (10+ year horizon), the answer is almost always yes. The best time to plant a tree was 20 years ago; the second best time is today. Every year of delay is a year of compounding permanently lost.

Should I invest in stocks or bonds as a beginner?

For most young investors with a long time horizon, a heavy stock allocation (80–100%) makes sense — stocks have higher long-term returns, and you have time to ride out volatility. As you approach a goal (retirement, home purchase), gradually shift toward bonds for stability.

What if the market crashes right after I invest?

This will likely happen at some point. If your time horizon is 10+ years, a crash in your first year is actually beneficial — your ongoing contributions buy more shares at lower prices, which compounds into greater wealth at recovery. The only way to be hurt is to sell. Don’t sell.

How do I know when to sell?

For index funds: almost never, except to rebalance or when you need the money. For individual stocks: when the fundamental investment thesis has changed, the business has deteriorated structurally, or the stock has become significantly overvalued relative to fair value. “The price fell” is never a reason to sell.

Every investor, at some point, will live through a stock market crash. The question isn’t whether it will happen — it’s whether you’ll be prepared when it does.

A stock market crash is a sudden, severe decline in stock prices — typically defined as a drop of 20% or more from recent highs, occurring rapidly over days or weeks. Crashes are distinct from bear markets (which can unfold slowly over months) in their speed and the panic they generate.

Understanding what causes crashes, how they’ve played out historically, and how to position yourself before, during, and after them is one of the most valuable skills a long-term investor can develop.

What Causes a Stock Market Crash?

Crashes rarely have a single cause. They typically involve a combination of overvaluation, leverage, and a triggering event that shatters confidence simultaneously across millions of investors.

The 5 Core Causes

Cause

Mechanism

Historical Example

Asset Bubble Bursting

Prices disconnected from fundamentals; sentiment reversal triggers mass selling

Dot-com crash 2000, Housing 2008

Economic Shock

Sudden external event destroys earnings expectations across broad sectors

Rapid rate hikes compress valuations; growth stocks most affected

1987 crash (rate fears), 2022 bear market

Panic and Contagion

Fear spreads faster than facts; investors sell first and ask questions later

Black Monday 1987, Flash Crash 2010

In practice, most crashes involve multiple causes reinforcing each other. The 2008 financial crisis combined a housing bubble, excessive leverage, a credit freeze, and widespread panic — each amplifying the others.

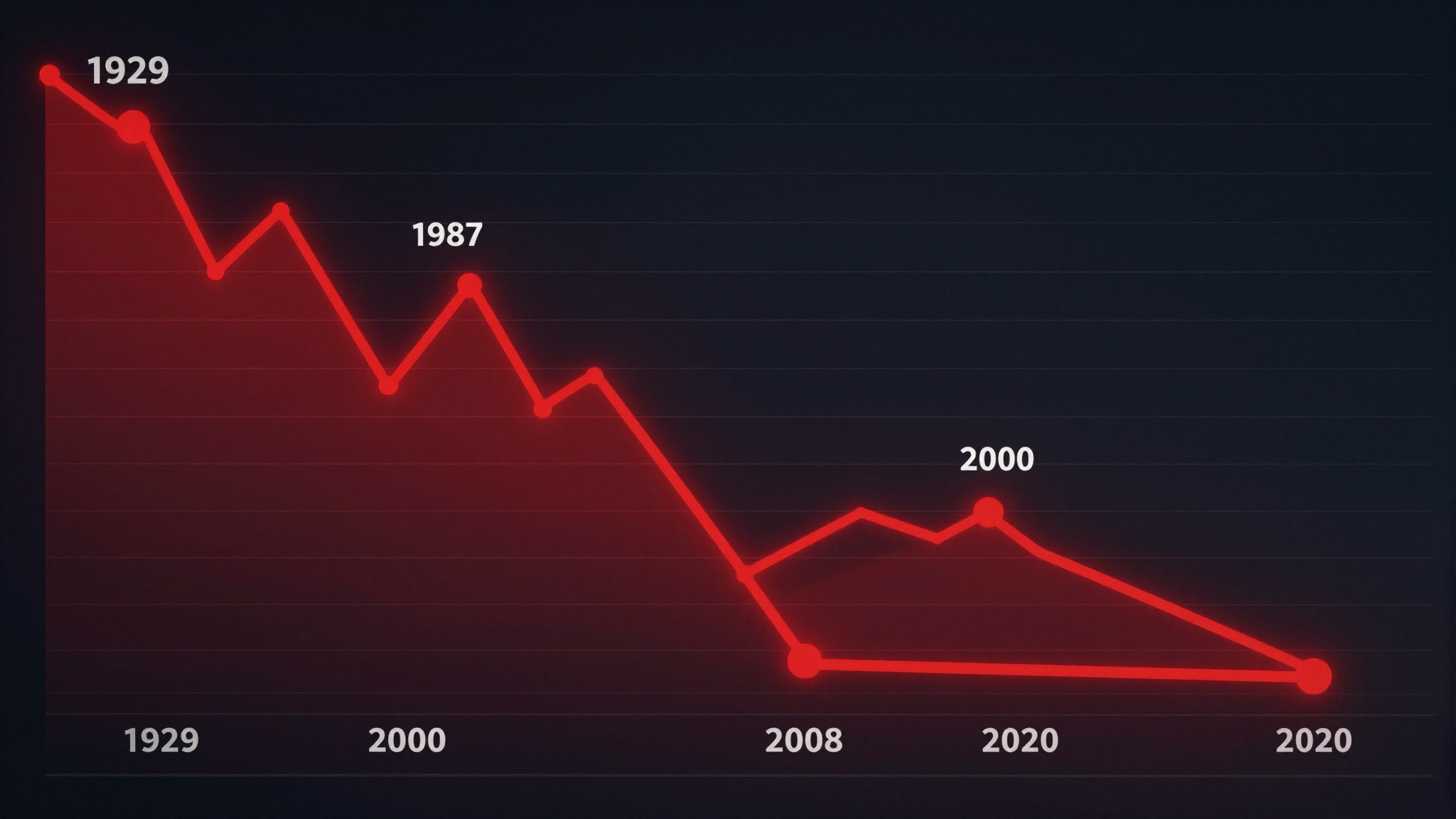

The 6 Major Crashes: What Happened and How Long Recovery Took

1. The Great Crash — 1929

Peak-to-trough decline: −89% (Dow Jones, 1929–1932) Recovery time: ~25 years to new highs

The defining crash of the 20th century. A decade of speculative excess, margin buying (investors borrowing 90% of purchase price), and bank failures created a collapse that took the Great Depression to fully manifest. The scale was historically unique — amplified by monetary policy mistakes and protectionist trade policies.

2. Black Monday — 1987

Single-day decline: −22.6% (Dow, October 19, 1987) Recovery time: ~2 years to new highs

The largest single-day percentage decline in Dow history. Triggered by rising interest rates, trade deficit concerns, and amplified by computer-driven “portfolio insurance” strategies that automatically sold as prices fell, creating a feedback loop. Markets recovered relatively quickly — the economy was fundamentally sound.

3. Dot-Com Crash — 2000–2002

Peak-to-trough decline: −78% (Nasdaq), −49% (S&P 500) Recovery time: ~7 years (S&P 500), Nasdaq took 15 years

The internet bubble inflated valuations of unprofitable companies to absurd levels. When profitability reality set in, the collapse was brutal — particularly for technology stocks. Companies with no earnings and astronomical P/E ratios fell 90–99%.

4. Global Financial Crisis — 2008–2009

Peak-to-trough decline: −57% (S&P 500) Recovery time: ~5.5 years to new highs

The most systemic crash since 1929. The collapse of the US housing market triggered a credit freeze that threatened the global banking system. Bear Stearns, Lehman Brothers, and AIG all failed or required emergency intervention. The Fed cut rates to zero and launched unprecedented quantitative easing.

5. COVID Crash — 2020

Peak-to-trough decline: −34% (S&P 500) in 33 days Recovery time: ~5 months — fastest recovery in history

The fastest crash in market history. Global lockdowns created an economic stop unlike anything seen before. But massive fiscal stimulus ($2T+ CARES Act), Federal Reserve intervention, and vaccine optimism produced an equally unprecedented recovery. Investors who sold at the bottom missed one of the strongest bull runs in decades.

Triggered by the fastest Fed rate-hiking cycle in 40 years to combat post-COVID inflation. Growth stocks and speculative assets (crypto, SPACs, unprofitable tech) fell dramatically — some 70–90% from peaks. Value and dividend stocks held up considerably better.

The Psychology of a Crash: Why Investors Make It Worse

Market crashes are as much psychological events as financial ones. Understanding the behavioral patterns that amplify crashes helps you avoid them.

The Panic Selling Loop

When prices fall sharply, fear triggers selling. Selling triggers more price declines. More price declines trigger more fear. This feedback loop can send markets well below any rational estimate of fundamental value — which is precisely why crashes create extraordinary buying opportunities for those who don’t panic.

Recency Bias

During a crash, investors extrapolate recent declines indefinitely into the future. “This will never recover” is the dominant narrative at market bottoms. In reality, every major crash in history has eventually been followed by new highs — including the Great Depression, though it took 25 years.

The Disposition Effect

Investors tend to sell winners quickly (to lock in gains) and hold losers too long (to avoid realizing losses). During crashes, this means they sell quality companies that have declined and hold onto speculative positions that may not recover.

The Crash Survival Playbook: 7 Rules

Rule 1: Do Nothing (If Your Portfolio Was Right Before)

The single most important crash rule. If you built a diversified, quality portfolio before the crash, the correct response to a 20–30% decline is almost always to do nothing. Selling locks in losses and removes you from the recovery.

The data is unambiguous: investors who stayed invested through every major crash since 1987 dramatically outperformed those who tried to time the market. Missing just the 10 best trading days in any given decade cuts long-term returns roughly in half.

Rule 2: Never Sell Because of Price Alone

Price is not a reason to sell. Business deterioration is. Ask the right question: Has the underlying business fundamentally changed, or has only the stock price changed? If your company is still generating cash, still has its competitive moat, and the reason you bought it is still intact — the crash has made it cheaper, not worse.

Rule 3: Rebalance Into Strength

Crashes are rebalancing opportunities. If equities have fallen from 70% to 55% of your target allocation (because prices dropped), buying stocks to restore your target allocation means systematically buying low. This is mechanically forced buying at depressed prices — exactly what you want.

Rule 4: Dollar-Cost Average Aggressively

Crashes are the best times to deploy regular investment contributions. The same $500/month buys significantly more shares at market lows than at highs. For a full framework on this strategy, see our guide on dollar-cost averaging.

Rule 5: Avoid Leverage Completely

Margin debt amplifies losses and introduces forced selling at the worst possible time. When prices fall, margin calls force you to sell — often at the exact bottom — regardless of your conviction in the investment. Crashes regularly bankrupt investors who were directionally correct but used leverage.

Rule 6: Keep Cash Reserves for Opportunities

Legendary investors — Buffett, Lynch, Templeton — consistently held cash reserves not as a defensive measure but as ammunition for crashes. A 10–15% cash position that you deploy during a 30% market decline can dramatically improve long-term returns. Crashes are not just risks to survive — they’re opportunities to exploit.

Rule 7: Have a Written Investment Policy

Write down your investment strategy, risk tolerance, and planned response to a 30% decline — before a crash happens. When markets are falling and every headline screams disaster, you will not make good decisions from scratch. A pre-written policy gives you something to execute mechanically, removing emotion from the process.

Why Crashes Create the Best Long-Term Buying Opportunities

The most counterintuitive truth in investing: crashes are good for long-term investors who don’t need their money immediately.

Crash

S&P 500 Return 1 Year After Bottom

S&P 500 Return 3 Years After Bottom

S&P 500 Return 5 Years After Bottom

1987 Black Monday

+23%

+53%

+91%

2002 Dot-com bottom

+29%

+61%

+82%

2009 Financial crisis

+69%

+98%

+178%

2020 COVID bottom

+75%

+89%

+110%*

*COVID 5-year return through 2025 estimated

In every case, investors who bought at the height of panic — when the news was worst and confidence was lowest — earned extraordinary returns in the years that followed. Crashes are the market’s clearance sales.

How to Position Your Portfolio Before a Crash

You can’t predict when a crash will come, but you can build a portfolio that survives one without requiring you to sell at the worst moment.

Quality over speculation: Companies with strong balance sheets, positive free cash flow, and durable competitive advantages fall less and recover faster. Speculative positions with no earnings often fall 70–90% and may not recover for a decade.

Avoid excessive leverage: No margin debt. If you can’t afford a 50% loss without being forced to sell, you have too much risk.

Maintain a cash buffer: 10–20% in cash or short-term bonds gives you both psychological comfort and buying power when opportunities appear.

Diversify across sectors: Healthcare, consumer staples, and utilities historically fall significantly less in crashes than technology and discretionary sectors.

Don’t over-concentrate in recent winners: The sectors that lead bull markets often lead crashes. Trim positions that have grown beyond your target allocation.

For a complete beginner framework on building a portfolio that can weather any market, see our guide on stock market for beginners, and for the step-by-step investing process, how to invest in stocks.

Common Questions About Stock Market Crashes

How often do stock market crashes happen?

Corrections (−10% or more) happen roughly every 1–2 years. Bear markets (−20% or more) occur approximately every 3–5 years. Severe crashes (−30%+) are rarer — roughly every 7–10 years. You will experience multiple major crashes in an investing lifetime. Accepting this as normal is the foundation of long-term investment success.

How long does it take to recover from a crash?

Recovery times vary enormously. The COVID crash recovered in 5 months; the Great Depression took 25 years. The average recovery from major bear markets since WWII is approximately 2–3 years. Crucially, these are total-return recoveries including dividends — which is why dividend reinvestment significantly accelerates recovery.

Should I sell everything before a crash?

Almost certainly not. To profit from this strategy, you’d need to correctly predict both when to sell and when to buy back — twice in a row. Research consistently shows that even professional investors can’t do this reliably. Investors who try to time crashes typically miss the recovery and end up worse off than if they’d done nothing.

Is a crash the same as a bear market?

Not exactly. A bear market is defined as a 20%+ decline from peak, which can unfold slowly over months. A crash implies speed — a rapid, panic-driven decline. The 2022 bear market unfolded over about 10 months; the 2020 crash reached −34% in 33 days. Both are painful; crashes are simply faster and more psychologically intense.

What’s the best investment during a crash?

Broadly, high-quality stocks with strong balance sheets and pricing power tend to hold up best. Defensives (healthcare, consumer staples, utilities) outperform in most crashes. Gold often performs well as a safe haven. Short-term Treasury bonds provide stability. Cash, while earning little, preserves capital and provides buying power. The “best” choice depends on your timeline and whether you’re preserving capital or seeking to deploy it.

When markets crash, when uncertainty spikes, when headlines scream about economic collapse — certain companies continue paying dividends, reporting profits, and serving customers as if nothing particularly dramatic is happening. These are blue chip stocks.

The term comes from poker, where blue chips carry the highest value. In investing, it describes companies that have earned that designation through decades of demonstrated resilience, financial strength, and market leadership. They’re not exciting. They rarely double overnight. But they form the foundation of portfolios built to last.

This guide covers what makes a company a true blue chip, which sectors produce the most reliable blue chips, how to evaluate them, and why they belong in every serious long-term portfolio — including how much weight to give them.

What Defines a Blue Chip Stock?

There’s no official list or regulatory definition of blue chip stocks, but the characteristics are well-understood by serious investors:

Market leadership — Dominant position in their industry, often with significant barriers preventing competitors from taking share

Long operating history — Typically 25–50+ years of continuous operation through multiple economic cycles

Large market capitalization — Generally $10 billion+, with many blue chips exceeding $100 billion

Consistent profitability — Earnings through recessions, not just in favorable conditions

Dividend track record — Most blue chips pay dividends and have raised them for years or decades consecutively

Global brand recognition — Names consumers and businesses around the world know and trust

The Dow Jones Industrial Average (DJIA) — the original 30 blue chip index — remains the most common benchmark for blue chip status, though today blue chips span far beyond those 30 names.

Why Blue Chip Stocks Belong in Every Portfolio

1. Resilience Through Recessions

Blue chip companies have survived and thrived through economic environments that destroyed lesser businesses. The 2000 dot-com crash, the 2008 financial crisis, the 2020 COVID shock — blue chips in consumer staples, healthcare, and utilities continued generating cash through all of them.

This isn’t accident. It reflects businesses selling products people need regardless of economic conditions (food, medicine, utilities), combined with financial strength (low debt, high cash flow) that allows them to weather downturns without existential risk.

2. Compounding Dividends Over Decades

Many of the most well-known blue chips — Johnson & Johnson, Procter & Gamble, Coca-Cola — have raised their dividends for 30–60+ consecutive years. An investor who bought Coca-Cola in 1990 at a 3% yield would today be receiving a yield-on-cost of over 20% annually based on the original purchase price.

This compounding effect — dividend growth on an appreciating asset — is the mechanism that makes blue chip investing extraordinarily powerful over 20–30+ year time horizons.

3. Lower Volatility (Behavioral Advantage)

Blue chips tend to fall less during market downturns and recover faster. Lower volatility isn’t just about math — it’s about behavior. Investors who watch their portfolio drop 50% in a growth stock crash often sell at the bottom. Investors holding blue chips that drop 20–25% and continue paying dividends are more likely to hold, or even add.

The behavioral advantage of a portfolio you can hold through turbulence is real and systematically undervalued by investors who focus only on theoretical return calculations.

Blue Chip Sectors: Where to Find Them

Blue chips cluster in industries with characteristics that produce durable competitive advantages and predictable cash flows.

Sector

Why It Produces Blue Chips

Representative Companies

Typical Dividend Yield

Consumer Staples

People buy food, beverages, and household products in every economic environment; strong brand pricing power

P&G, Coca-Cola, PepsiCo, Unilever, Colgate

2–4%

Healthcare

Aging demographics, patent-protected products, inelastic demand for medicine and devices

Johnson & Johnson, Abbott, Medtronic, Merck, Pfizer

2–4%

Financials

Essential intermediaries; well-capitalized banks and insurers survive cycles others don’t

Mature tech leaders with dominant platforms, high switching costs, and enormous cash generation

Microsoft, Apple, Alphabet, Oracle

0.5–2%

Industrials

Diversified businesses with global infrastructure exposure; capital allocation discipline over decades

3M, Caterpillar, Honeywell, Illinois Tool Works

2–4%

Utilities

Regulated monopolies with predictable cash flows and government-mandated services

Duke Energy, Southern Company, NextEra Energy

3–5%

How to Evaluate a Blue Chip Stock

Because blue chips are widely known and followed by hundreds of analysts, they’re rarely dramatically mispriced. The evaluation task isn’t finding hidden value — it’s determining whether you’re paying a fair or excessive price for exceptional quality.

Key Metrics for Blue Chip Analysis

Metric

What to Check

Strong Blue Chip Signal

Dividend Growth Rate (5-year)

Annual rate of dividend increases

5%+ consistently; ideally 8–10%

Payout Ratio

Dividends ÷ Earnings

Below 60% — room to grow without straining earnings

Return on Equity (ROE)

Net Income ÷ Shareholders’ Equity

Above 20% sustained over 5+ years

Debt-to-EBITDA

Total Debt ÷ EBITDA

Below 2.5× — conservative leverage

Credit Rating

S&P / Moody’s / Fitch rating

A or above; AA for strongest blue chips

Consecutive Dividend Years

Years of uninterrupted dividend increases

25+ years (Aristocrat), 50+ (King)

Gross Margin Trend

Gross profit margin over 5 years

Stable or expanding; above 40% for most

Valuation: The Price You Pay Matters Even for Blue Chips

Blue chips command premium valuations — they should. Predictable earnings, long dividend track records, and balance sheet strength justify higher multiples than average businesses.

But “premium business” doesn’t mean “pay any price.” Buying blue chips at extreme valuations (P/E of 35–40× for businesses growing earnings at 5–7%) produces mediocre returns even when the business itself continues to perform well.

Fair value framework for blue chips:

P/E: Compare to the company’s own 10-year average and current sector median. Buying at or below historical average P/E generally produces good results.

Dividend yield: When a blue chip’s yield is above its 5-year average, it often signals the stock is undervalued relative to its history.

PEG ratio: A PEG below 2.0 is reasonable for high-quality blue chips; below 1.5 represents good value.

Building a Blue Chip Core Portfolio

For most long-term investors, blue chips serve as the stable core around which higher-risk positions are built. A common framework:

Growth stocks, sector leaders in emerging industries

Opportunistic

10–20%

Higher-risk/reward bets with time-limited thesis

Small caps, cyclicals at trough, turnarounds

This core-satellite structure — which we cover in detail in our pillar guide on stock investment strategies — uses blue chips to anchor the portfolio’s risk profile while allowing participation in higher-upside opportunities.

Blue Chip ETFs: The Passive Route

If building a diversified blue chip portfolio stock-by-stock feels complex, ETFs offer a low-cost shortcut:

ETF

Focus

Yield (~)

Expense Ratio

DIA — SPDR Dow Jones Industrial Average

30 Dow blue chips directly

~1.8%

0.16%

NOBL — ProShares S&P 500 Dividend Aristocrats

25+ year dividend growers

~2.1%

0.35%

VIG — Vanguard Dividend Appreciation

10+ year dividend growers, quality screen

~1.8%

0.06%

SCHD — Schwab US Dividend Equity

Quality + yield hybrid, strong blue chip tilt

~3.4%

0.06%

XLP — Consumer Staples Select Sector SPDR

Pure consumer staples exposure

~2.8%

0.09%

The Trade-Offs of Blue Chip Investing

Blue chips are excellent — but they’re not a free lunch. Understanding the trade-offs prevents unrealistic expectations.

Advantage

Trade-Off

Recession resilience

Modest upside in strong bull markets

Reliable dividend income

Yields rarely exceed 4–5%; not high income

Lower volatility

Less excitement; hard to generate 10× returns

Widely researched

Rarely dramatically mispriced; limited alpha

Global brand recognition

Size makes hypergrowth structurally difficult

The bottom line: blue chips are not the path to getting rich quickly. They are the path to staying rich, compounding steadily, and sleeping well during the inevitable market turbulence that derails less disciplined investors.

Common Questions About Blue Chip Stocks

Are blue chip stocks safe to hold forever?

Generally safer than average stocks — but “forever” is too absolute. Blue chip status isn’t permanent. Kodak, Sears, and General Electric were once definitive blue chips. Businesses that fail to adapt to structural industry changes can lose their position over decades. The solution is periodic portfolio review — not constant trading, but checking every 1–2 years that the core thesis (moat, financial strength, dividend sustainability) remains intact.

Should beginners start with blue chip stocks?

Yes — they’re often the ideal starting point. Lower volatility means less emotional stress during learning. Consistent dividends provide feedback that the investment is working. And the research process for blue chips (reading annual reports, understanding competitive advantages) builds skills that transfer to evaluating more complex opportunities later.

How many blue chip stocks should I own?

A portfolio of 15–25 blue chips across 5–6 sectors provides meaningful diversification while remaining manageable. Beyond 30 individual stocks, monitoring becomes burdensome and returns tend to converge toward index performance anyway.

Are blue chip stocks good for retirees?

They’re often ideal for the equity portion of a retirement portfolio. The combination of dividend income (which can partially fund living expenses without selling shares) and lower volatility (which reduces sequence-of-returns risk) aligns well with retirement needs. Many retirees hold a core of 15–20 blue chips alongside bonds and cash.

What happened to blue chip stocks in 2008?

Most fell significantly — a broad market crash affects virtually everything. But the strongest blue chips (consumer staples, healthcare, utilities) fell less (20–35%) versus the S&P 500’s 57% peak-to-trough decline. More importantly, they continued paying and growing dividends throughout the crisis, and recovered faster than the broader market. The 2008 experience reinforced, rather than undermined, the case for blue chip quality.

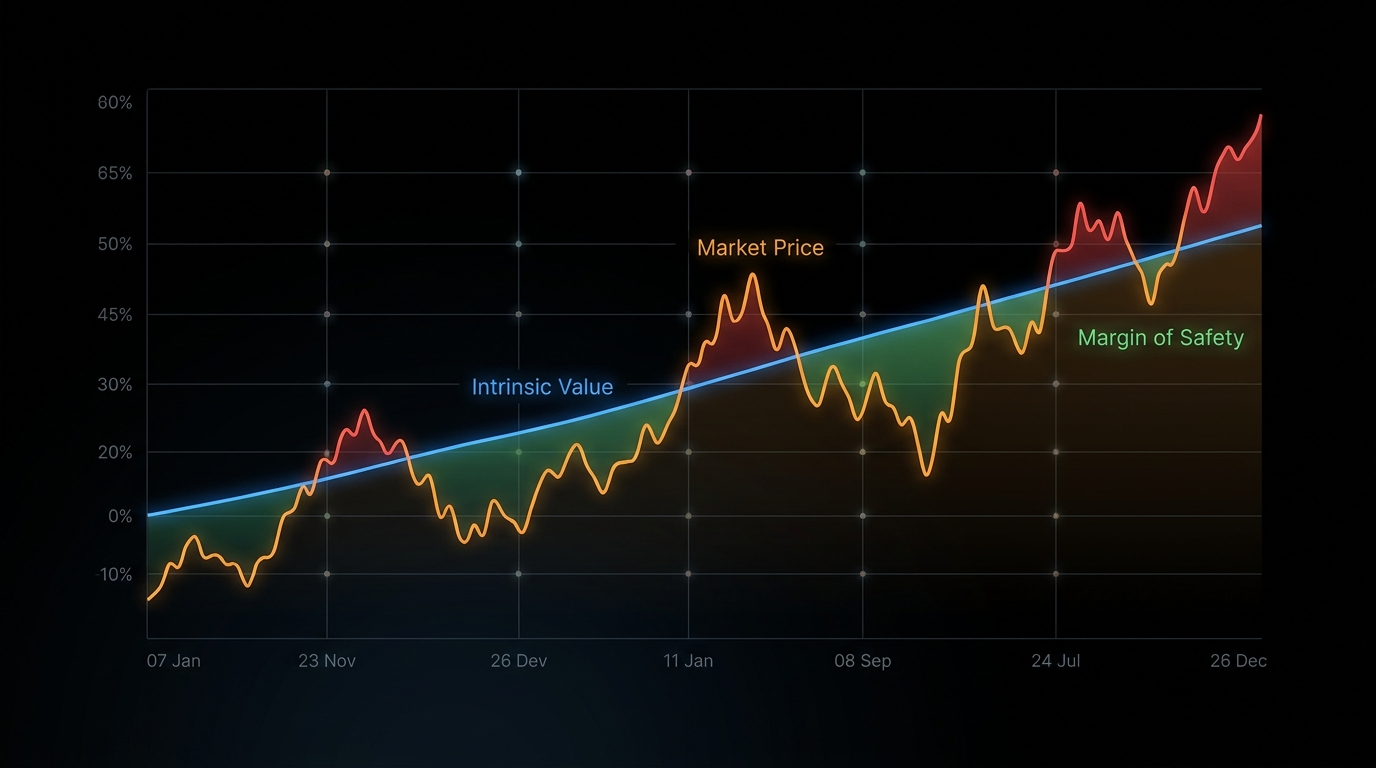

Every great investment has one thing in common: the price paid was lower than what the asset was actually worth. That gap — between price and value — is the entire foundation of finding undervalued stocks.

The concept sounds simple. The execution is where most investors struggle. Markets are reasonably efficient most of the time, which means obvious bargains are rare and quickly arbitraged away. But markets are also driven by emotion, narrative, and short-term thinking — which creates persistent mispricings for investors patient enough to look past the noise.

This guide covers four proven methods for identifying stocks trading below intrinsic value, how to distinguish a genuine bargain from a value trap, and the mental framework that separates successful value hunters from investors who buy cheap stocks that get cheaper.

What Makes a Stock “Undervalued”?

A stock is undervalued when its current market price is lower than the present value of the future cash flows the underlying business will generate. This is the core definition — and it immediately tells you that “undervalued” is not about a stock’s price in isolation.

A $5 stock is not inherently cheap. A $500 stock is not inherently expensive. Price alone means nothing. What matters is what you get for that price — the quality and predictability of the earnings, cash flows, and assets backing it.

Common reasons stocks become undervalued:

Temporary bad news — A missed earnings quarter, a product recall, a management departure. Markets often overreact to short-term events in businesses with long-term durable fundamentals.

Sector rotation — Investors collectively move away from certain industries (energy, banks, utilities) regardless of individual company fundamentals, creating bargains for those willing to look.

Complexity discount — Businesses with convoluted structures (holding companies, conglomerates, spinoffs) are often ignored by analysts, leaving them mispriced by the market.

Small cap neglect — Smaller companies receive less analyst coverage, creating more room for mispricings that diligent individual investors can exploit.

Market-wide panic — Broad sell-offs (2008, 2020, 2022) push even high-quality businesses to temporarily irrational prices.

The 4 Methods for Finding Undervalued Stocks

Method 1: The Earnings-Based Screen (P/E and PEG)

The price-to-earnings (P/E) ratio is the most widely used valuation metric — and the most frequently misused. The right way to use P/E is not to find stocks with “low numbers,” but to find stocks whose P/E is low relative to their earnings quality and growth rate.

How to apply P/E correctly:

Compare P/E to the company’s own 5-year historical average — is it trading at a discount to its own history?

Compare P/E to sector peers — is it cheaper than comparable businesses for a reason that’s temporary or structural?

Use the PEG ratio (P/E ÷ earnings growth rate) to adjust for growth. A PEG below 1.0 often signals undervaluation; above 2.0 signals potential overvaluation.

Metric

Formula

Undervalue Signal

Watch Out For

P/E Ratio

Price ÷ EPS

Below sector average + company history

Cyclical earnings can make P/E look misleadingly low at peaks

Forward P/E

Price ÷ Next Year EPS estimate

Below 15× for stable businesses

Estimates can be wrong — verify revenue trends

PEG Ratio

P/E ÷ 5-year EPS growth rate

Below 1.0

Growth projections can be overly optimistic

Normalized P/E

Price ÷ 10-year average EPS

Below historical norms for that sector

Best for cyclical industries to smooth out peaks/troughs

Method 2: The Asset-Based Screen (P/B and NAV)

Price-to-book (P/B) compares a stock’s market price to the net asset value (book value) on the company’s balance sheet. When P/B falls below 1.0, you’re theoretically paying less than the liquidation value of the company’s assets.

When P/B is most useful:

Banks and financial institutions (assets are primarily financial, book value is meaningful)

Real estate companies and REITs (property values can be estimated independently)

Industrial and manufacturing companies with significant tangible assets

When P/B is less useful:

Technology and software companies (most value is in intangibles: patents, brand, code — not on the balance sheet)

Service businesses where people are the primary asset

The Net-Net Screen (Benjamin Graham’s Method)

Graham’s classic approach looked for stocks trading below “net current asset value” — current assets minus all liabilities. If you could buy a business for less than its working capital (cash, receivables, inventory) with zero value assigned to fixed assets, you had a margin of safety even in a worst-case scenario.

True net-nets are extremely rare today in major markets. But the principle — demanding a substantial discount to tangible asset value — remains sound, particularly in small-cap and international markets.

Method 3: The Cash Flow-Based Screen (P/FCF and EV/EBITDA)

Free cash flow is the lifeblood of a business — it’s what remains after maintaining and growing operations. Unlike earnings, free cash flow is harder to manipulate through accounting choices. P/FCF (price-to-free-cash-flow) and EV/EBITDA are therefore often more reliable signals of undervaluation than P/E alone.

P/FCF: Divide the stock price by free cash flow per share. A P/FCF below 15× in most sectors suggests reasonable value; below 12× often signals undervaluation relative to cash generation.

EV/EBITDA: Enterprise Value ÷ EBITDA. EV accounts for debt and cash, making it a better apples-to-apples comparison across companies with different capital structures. Below 8–10× is often considered undervalued for stable businesses.

FCF Yield: The inverse of P/FCF (FCF per share ÷ stock price × 100). An FCF yield above 6–8% in a low-interest-rate environment is compelling; it means the business generates real cash equivalent to 6–8% of your investment annually before any price appreciation.

Method 4: The Dividend Yield Signal

For established dividend-paying companies, yield can serve as a valuation proxy. When a stock’s dividend yield is significantly above its historical average, it often indicates the price has fallen more than the business fundamentals justify.

The logic: if a company pays $2/share annually and the stock falls from $50 (4% yield) to $35 (5.7% yield), one of two things is true: either the business has genuinely deteriorated, or the market has overreacted to temporary concerns. Distinguishing between the two is the research task.

Dividend yield signals work best for: Utilities, consumer staples, financials, and REITs — sectors with predictable, regulated, or structurally stable cash flows where management has a long-term commitment to the dividend.

For a deeper dive into dividend-based investing, see our guide on dividend investing.

The Value Trap: How to Avoid Buying a Cheap Stock That Gets Cheaper

The most dangerous concept in value investing is the value trap — a stock that looks cheap by every metric but continues to fall (or stays flat for years) because the underlying business is in structural decline.

Classic value traps share several characteristics:

Industry in secular decline — Print media, legacy retail, traditional telecoms. Low P/E can persist for years as earnings gradually erode.

Competitive advantage has eroded — What was once a moat has been bridged. The “cheap” valuation reflects a market that recognizes the deterioration before the investor does.

Debt is high relative to declining cash flows — A leveraged balance sheet amplifies the damage when business conditions worsen.

Management is in denial — Earnings calls emphasize “challenging environment” rather than addressing structural problems with a credible plan.

The key question that separates undervalued from value trap:

Is the business worth less intrinsically, or has the market temporarily mispriced a fundamentally sound business?

Temporary mispricings recover when the cause of the sell-off resolves. Structural deterioration doesn’t recover — it just gets incrementally worse as the moat widens against the company.

A Practical Screening Workflow for Undervalued Stocks

Step 1: Quantitative Screen

Use a stock screener (Finviz, Simply Wall St., or your broker) with these filters:

P/E below sector median

P/FCF below 20×

EV/EBITDA below 10×

Positive free cash flow for last 3 years

Debt-to-equity below 1.5

ROE above 12% (quality filter — ensures low price isn’t due to poor profitability)

Step 2: Catalyst Check

For each stock that passes the screen, identify: why is this cheap, and what could change the market’s perception?

Without a credible catalyst — an upcoming product launch, a cyclical recovery, a management change, a spinoff or restructuring — cheap stocks can stay cheap indefinitely. A catalyst doesn’t need to be imminent, but it should be identifiable.

Step 3: Intrinsic Value Estimate

Run a conservative DCF (discounted cash flow) or comparable company analysis to estimate what the business is actually worth. Build in a margin of safety — buy only when the stock is trading at least 20–30% below your intrinsic value estimate.

Step 4: Thesis Documentation

Write down your investment thesis in 3–5 sentences: why you think the stock is undervalued, what the catalyst for re-rating is, and what would make you wrong. This discipline prevents emotional decision-making later — either anchoring to a losing position or selling a winning one prematurely.

Where to Find Undervalued Stocks

Beyond screeners, several sources consistently surface overlooked or mispriced opportunities:

52-week low lists — Stocks near 52-week lows have often been through institutional selling. Some are value traps; others are overreactions to temporary news.

Recent spinoffs — When a conglomerate spins off a division, institutional investors often automatically sell the new entity (it doesn’t fit their mandate). This forced selling creates temporary mispricings.

Insider buying activity — SEC Form 4 filings show when executives buy their own stock in the open market. Multiple insiders buying during a price decline is a meaningful signal.

Neglected sectors — Sectors that have underperformed for 2–3 years accumulate bargains as investors rotate away. Energy in 2020, financials in 2023, and consumer staples in 2024 all offered opportunities after extended periods of underperformance.

Undervalued Stock Metrics at a Glance

Method

Primary Metric

Signal Level

Best For

Earnings-based

P/E, PEG

P/E below sector; PEG below 1.0

Stable, profitable businesses

Asset-based

P/B, P/NAV

P/B below 1.5× for non-tech

Financials, industrials, real estate

Cash flow-based

P/FCF, EV/EBITDA

P/FCF below 15×; EV/EBITDA below 10×

Most sectors; especially capital-light

Yield-based

Dividend yield vs history

Yield significantly above 5-year average

Utilities, consumer staples, REITs, banks

Common Questions About Undervalued Stocks

How long does it take for an undervalued stock to recover?

There’s no fixed timeline — this is one of the hardest aspects of value investing. Some mispricings resolve in months; others take 2–3 years. Keynes’ observation that markets can stay irrational longer than you can stay solvent is a real risk. This is why position sizing and patience are essential, and why buying near a catalyst (rather than purely on cheapness) improves outcomes.

Are there always undervalued stocks in the market?

In a bull market with high valuations, genuine bargains are rare. In corrections and bear markets, they’re widespread. The best times to build a position in undervalued stocks are precisely the times when fear is highest — which requires emotional discipline most investors struggle with.

Is a low P/E ratio enough to identify undervalued stocks?

No. P/E alone is one of the least reliable valuation signals in isolation. Low P/E stocks can reflect poor earnings quality, cyclical peak earnings about to decline, or structural business deterioration. Always combine P/E with FCF analysis, balance sheet quality checks, and a qualitative assessment of business durability.

What’s the difference between undervalued and cheap?

“Cheap” refers to price. “Undervalued” refers to the relationship between price and intrinsic value. A $3 penny stock can be expensive if it’s worth $0.50. A $1,000 stock can be cheap if it’s worth $1,500. The language matters — train yourself to always think in terms of value relative to price, not price in isolation.

For a comprehensive framework on selecting the best individual stocks, see our pillar guide on best stocks to invest in. And if you’re evaluating stocks using a quantitative picking process, our guide on how to pick stocks covers the full 5-step methodology.

Most investors approach stock picking backwards. They hear about a company — on social media, from a friend, in a news headline — and then go looking for reasons to buy. The decision comes first; the analysis comes after, deployed in service of a conclusion already reached.

This is precisely why most individual investors underperform the market. It’s not a lack of intelligence or access to information. It’s a flawed process.

How to pick stocks the right way means inverting that process entirely: start with a framework, run the numbers, and let the evidence lead you to a conclusion — rather than working backwards from excitement. This guide gives you that framework, step by step.

Why Stock Picking Is Hard (and When It’s Worth Trying)

Before diving into the process, an honest caveat: beating the market consistently is genuinely difficult. Professional fund managers — with teams of analysts, proprietary data, and decades of experience — fail to outperform low-cost index funds over 10+ year periods the majority of the time.

That doesn’t mean individual stock picking is pointless. It means going in with clear eyes about the challenge. Stock picking makes sense when:

You have genuine insight into an industry or business that the broader market doesn’t fully appreciate

You’re willing to do real research — reading earnings reports, understanding competitive dynamics, tracking management quality

You have a long enough time horizon (3–5+ years minimum) for your thesis to play out

You can hold through volatility without panicking when the stock drops 20%

If those conditions don’t apply, low-cost index funds are the rational default. But if you’re committed to individual selection, the framework below gives you the best structural approach.

The 5-Step Framework for Picking Stocks

Step 1: Define Your Investment Universe

The stock market contains thousands of companies. Trying to evaluate all of them is impossible. The first step is narrowing to a manageable universe based on your knowledge and criteria.

Start with what you know. Peter Lynch, one of the most successful fund managers in history, made “invest in what you know” famous — not as a license to buy any company whose products you use, but as a starting point for identifying businesses you can actually understand.

If you work in healthcare, you may understand drug approval processes, hospital procurement decisions, and competitive dynamics that a generalist investor misses. That’s a legitimate edge. Lean into it.

Apply basic filters to shrink the universe:

Market cap above $1 billion (smaller companies are harder to research and less liquid)

Minimum 3 years of operating history

Sector you understand or are willing to learn deeply

Listed on major exchanges (NYSE, NASDAQ) for liquidity and disclosure quality

Step 2: Evaluate Business Quality

Before looking at a single financial metric, answer this question: Is this a good business?

A good business has durable competitive advantages — what Warren Buffett calls a “moat” — that protect it from competition and allow it to earn above-average returns on capital over time.

The 5 types of economic moats:

Moat Type

Description

Example Companies

Network Effects

Product becomes more valuable as more people use it

Visa, Mastercard, Meta

Switching Costs

Customers face high cost or friction to switch to a competitor

Salesforce, Oracle, Adobe

Cost Advantages

Can produce at lower cost than competitors due to scale, location, or process

Serves a niche market that isn’t attractive enough for new entrants

Many utilities, rail operators

A business without a moat can still be profitable — but its profits are always at risk from a well-funded competitor. With a moat, it can sustain excess returns for years or decades.

Step 3: Analyze Financial Health

Once you’ve confirmed business quality, dig into the numbers. You’re looking for evidence that the business generates real cash, isn’t drowning in debt, and is becoming more profitable over time — not just growing revenue.

Below 2× — debt could become a crisis in a downturn

Pro tip: Don’t just look at the latest quarter. Pull 5 years of data and look at the trend. A company with 15% ROE that’s been declining from 25% is a very different story from one that’s growing from 10%.

Step 4: Assess Management Quality

A great business with poor management will eventually underperform. A mediocre business with exceptional management can sometimes overcome its structural disadvantages. Management assessment is qualitative, but there are concrete signals to look for.

Signs of good management:

Capital allocation track record — Do they invest in high-return projects or make empire-building acquisitions that destroy value?

Insider ownership — Management that owns significant personal stakes has skin in the game. Check SEC filings for ownership levels and recent buy/sell activity.

Guidance accuracy — Do they consistently deliver on what they promise? Look at 2–3 years of earnings calls and compare guidance to actual results.

Compensation structure — Are executives paid based on metrics that align with shareholder value (ROIC, FCF per share) or metrics that are easy to game (revenue, adjusted EBITDA)?

Honest communication — Do they talk openly about challenges and mistakes, or does every earnings call sound like an infomercial?

Where to research management: Annual reports (especially the shareholder letters), earnings call transcripts (available on Seeking Alpha or the company’s IR site), and SEC proxy statements (DEF 14A) for compensation and insider ownership.

Step 5: Evaluate Valuation

A wonderful company at a terrible price is still a bad investment. The final step is determining whether the current stock price gives you an adequate margin of safety — room for error in your analysis, and potential upside if your thesis plays out.

The most useful valuation metrics:

Metric

Formula

Use When

Benchmark

P/E Ratio

Price ÷ Earnings per Share

Profitable, stable companies

Compare to sector average and historical range

P/FCF Ratio

Price ÷ Free Cash Flow per Share

Companies with high non-cash charges

Below 20× is often reasonable

EV/EBITDA

Enterprise Value ÷ EBITDA

Capital-intensive businesses, comparing across cap structures

Below 10–12× often indicates value

PEG Ratio

P/E ÷ Earnings Growth Rate

Growth companies

Below 1.0 often indicates undervaluation

Price-to-Book

Price ÷ Book Value per Share

Financials, asset-heavy industries

Below 1.5× often indicates value; vary widely by sector

Important: No single metric tells the whole story. A stock trading at P/E 30 might be cheap if it’s growing earnings at 40% annually. A stock at P/E 10 might be expensive if earnings are about to collapse. Always triangulate across multiple metrics and compare to peers and the company’s own history.

The concept of intrinsic value: Many serious investors estimate a business’s intrinsic value using discounted cash flow (DCF) analysis — projecting future free cash flows and discounting them back to present value. DCF is powerful but sensitive to assumptions. Use it as a directional tool, not a precise answer.

Building a Stock Screening Workflow

The 5-step framework above works best when applied systematically. Here’s a practical workflow for finding and evaluating stocks efficiently.

Phase 1: Quantitative Screen (5–10 minutes per stock)

Use a free screener (Finviz, Macrotrends, or your broker’s tools) to filter the universe down to candidates that pass basic quality tests:

Revenue growth (3-year CAGR) > 5%

Gross margin > 30%

Free cash flow positive for last 3 years

Return on equity > 12%

Debt-to-equity < 1.5

P/E or P/FCF below 30× (adjust for sector)

Phase 2: Qualitative Deep Dive (1–3 hours per stock)

For companies that pass the quantitative screen:

Read the most recent annual report (10-K) — especially the Business and Risk Factors sections

Listen to or read 2–3 recent earnings call transcripts

Identify the moat — what protects this business from competition?

Check insider ownership and recent transactions (SEC EDGAR)

Read one or two analyst reports for alternative perspectives (not as gospel, but as a check)

Phase 3: Valuation Check (30–60 minutes)

Calculate P/E, P/FCF, and EV/EBITDA vs. sector peers

Compare current valuation to the company’s 5-year historical range

Run a simple DCF with conservative assumptions

Define your margin of safety — how much downside is acceptable if you’re wrong?

Common Stock Picking Mistakes to Avoid

1. Buying on a Story Without the Numbers

A compelling narrative — “this company is disrupting a $500B market” — is not an investment thesis. Great stories built on weak financials regularly end in 80%+ losses. The story is the starting point for research, not the conclusion.

2. Confusing a Good Company with a Good Stock

Apple, Amazon, and Google are all exceptional businesses. But if you bought Apple in late 2007 at peak valuation before the financial crisis, you’d have waited years to break even. Valuation matters — even for the best companies.

3. Over-Diversifying (Diworsification)

Owning 50 stocks is not necessarily better than owning 20. Beyond a certain point, diversification dilutes your best ideas while adding the complexity of tracking dozens of positions. Most professional investors consider 15–25 stocks optimal for a concentrated individual portfolio.

Insiders sell for many reasons (liquidity needs, tax planning, estate planning). A single insider sale rarely signals trouble. But a pattern of heavy selling across multiple executives — especially when accompanied by secondary offerings — warrants serious attention. Insider buying, however, is a more unambiguous signal: the only reason to buy your own stock is if you think it’s going up.

5. Not Having a Sell Discipline

Most investors spend 95% of their time thinking about what to buy and almost no time thinking about when to sell. Define your sell criteria before you buy: What would make this thesis wrong? At what price would the stock be overvalued? Having explicit sell rules prevents emotional decision-making in both directions.

Stock Picking vs. Index Investing: A Realistic Comparison

Factor

Stock Picking

Index Investing

Time required

High — ongoing research

Minimal — set and monitor

Potential outperformance

Possible with skill + edge

Market return (minus fees)

Risk of underperformance

Significant — most active strategies lag

Cannot underperform by definition

Tax efficiency

Can optimize via timing

Very efficient (low turnover)

Intellectual engagement

High — ongoing learning

Low — largely passive

Behavioral challenge

High — requires discipline not to react

Lower — fewer decisions to make

The honest conclusion: for most people, most of the time, low-cost index funds are the better choice. But for investors who enjoy the research process, have genuine industry knowledge, and can maintain discipline over long periods, individual stock picking can be rewarding both financially and intellectually.

The key is knowing which category you’re in — and being honest about it.

Putting It All Together: Your Stock Picking Checklist

✅ Do I understand how this business makes money?

✅ Does the company have a durable competitive moat?

✅ Is revenue growing consistently over 3–5 years?

✅ Is free cash flow positive and growing?

✅ Is the payout ratio or debt level manageable?

✅ Does management have skin in the game?

✅ Is the stock trading below my estimate of intrinsic value?

✅ What would make this thesis wrong — and am I comfortable with that risk?

✅ Do I have a sell plan if the business deteriorates or the stock becomes overvalued?

Stock picking is not about finding sure things — there are none. It’s about building a repeatable process that gives you an edge over emotional, story-driven investors who buy first and ask questions later. Follow the framework, do the work, and the results tend to take care of themselves.

For a framework on which specific types of stocks to target, see our guide on best stocks to invest in — which covers the 5-Factor selection model in detail. And if you’re evaluating a stock trading below its perceived value, our deep-dive on value investing covers the full methodology.

Every quarter, millions of investors wake up to find money sitting in their brokerage accounts — money they didn’t earn by working, trading, or making any decision at all. Their stocks simply paid them.

That’s the core promise of dividend investing: own pieces of businesses that share their profits with you, regularly and predictably, for as long as you hold them.

It sounds almost too simple. And in many ways, it is simple — but not easy. The difference matters. Getting dividend investing right means understanding which yields to trust, how dividends compound over time, and why chasing the highest payout is often the fastest path to losing both the income and the principal.

This guide covers everything: how dividends work mechanically, what separates a sustainable dividend from a yield trap, how to build a portfolio designed for growing income, and the metrics that actually predict dividend reliability.

What Is a Dividend — and Why Do Companies Pay Them?

A dividend is a cash distribution a company pays to shareholders, typically from its profits. When you own 100 shares of a company paying $2 per share annually, you receive $200 per year — regardless of what the stock price does on any given day.

Most U.S. companies pay dividends quarterly. Some pay monthly (REITs and certain funds). A few pay annually or semi-annually, more common outside the U.S.

Why Companies Pay Dividends

Mature businesses with more cash than reinvestment opportunities — A utility company can’t build an infinite number of power plants. The excess cash goes to shareholders.

Shareholder return programs — Boards use dividends to compete for income-focused investors, particularly institutional funds with income mandates.

Signaling confidence — A management team willing to commit to a dividend is implicitly saying: “We’re confident in our future earnings.” Cutting a dividend is painful and publicly embarrassing — so companies only start one if they believe they can sustain it.

The 4 Critical Dates Every Dividend Investor Must Know

Date

What It Means

Why It Matters

Declaration Date

Board announces the dividend amount and payment schedule

First confirmation of the payout

Ex-Dividend Date

First day you must already own shares to receive the dividend

Buy on or after this date → you don’t get paid this cycle

Record Date

Company takes a snapshot of shareholders on its books

Usually 1 business day after ex-date

Payment Date

Cash actually hits your account

Typically 2–4 weeks after ex-date

Key rule: You must own the stock before the ex-dividend date to receive the upcoming dividend. Buying on the ex-date means you’ll wait for the next cycle.

How Dividend Investing Actually Generates Wealth

Dividends generate returns in two ways that compound on each other over time.

1. Cash Income (The Obvious Part)

If you own $100,000 in dividend stocks yielding 3.5%, you collect $3,500 per year in cash. That’s $292 per month arriving in your account whether markets are up, down, or sideways.

2. Dividend Reinvestment (The Compounding Engine)

When you reinvest dividends — using each payment to buy more shares — your position compounds automatically. More shares = more dividends = even more shares. This is the mechanism behind one of the most quoted statistics in investing:

Dividend reinvestment has historically accounted for roughly 40% of the S&P 500’s total returns over long periods. The price appreciation gets the headlines; reinvested dividends do much of the actual work.

The Math of Dividend Reinvestment Over 20 Years

Scenario

Starting Investment

Annual Yield

Price Growth

20-Year Value

No dividends

$50,000

0%

7%

$193,484

Dividends taken as cash

$50,000

3%

5%

$132,665 + $58,200 cash

Dividends reinvested

$50,000

3%

5%

$261,743

The 5 Core Metrics for Evaluating Dividend Stocks

Not all dividends are created equal. These five metrics separate sustainable dividends from payout traps.

1. Dividend Yield

Formula: Annual Dividend Per Share ÷ Current Stock Price × 100

If a stock pays $2 annually and trades at $50, the yield is 4%.

Danger zone: Yields above 6–7% in most sectors warrant serious investigation. High yield is sometimes a warning signal, not a reward.

2. Dividend Payout Ratio

Formula: Annual Dividends Per Share ÷ Earnings Per Share × 100

Payout Ratio

Signal

Context

Under 40%

Very conservative

Plenty of room to raise dividend, strong safety margin

40–60%

Balanced

Typical for established dividend payers

60–80%

Moderate concern

Less flexibility; watch earnings trends closely

Over 80%

Elevated risk

Any earnings weakness could force a cut

Over 100%

Paying from debt or reserves

Unsustainable unless company has a plan to fix it

Exception: REITs use FFO (Funds from Operations) rather than GAAP earnings. Payout ratios of 70–90% based on FFO are normal and often healthy for REITs.

3. Dividend Growth Rate

A company that raised its dividend by 8% per year for the last 10 years is usually more valuable to a long-term investor than one offering a 6% yield with flat growth.

Why growth matters: Assume you bought a stock 10 years ago yielding 2.5%. If it grew dividends at 10% annually, your yield-on-cost today is roughly 6.5% — based on what you originally paid. This is the real power of dividend growth investing.

4. Free Cash Flow Coverage

Earnings can be manipulated. Free cash flow (operating cash flow minus capital expenditures) is harder to fake — it’s real money in the bank.

Always check FCF coverage alongside the reported payout ratio, especially for capital-intensive businesses.

5. Dividend Track Record

Dividend Aristocrats — S&P 500 companies that have raised dividends for 25+ consecutive years (67 companies as of 2024)

Dividend Kings — Companies with 50+ consecutive years of dividend increases (fewer than 55 companies qualify)

The 4 Main Dividend Investing Strategies

Strategy 1: High-Yield Income Investing

Goal: Maximum current income | Typical yield target: 4–7%+ | Best for: Retirees who need income now

Screening filters:

Yield 4–7% (anything above 7% requires extra scrutiny)

Payout ratio under 75%

Positive free cash flow

Debt-to-equity below 2.0

At least 5 years of maintained or growing dividends

Strategy 2: Dividend Growth Investing

Goal: Lower yield now, rapidly growing income over time | Typical yield target: 1.5–3.5% | Best for: Younger investors building toward future income

A stock yielding 2% that grows dividends at 10% per year will yield roughly 5.2% on your original investment in 10 years and 13.5% in 20 years.

Strategy 3: DRIP Investing

Goal: Automatic compounding | Best for: Hands-off investors